Behind Zepto's ₹12,000 Cr. IPO.

The company is betting on something no other player really is.

Blinkit turned profitable in 2025. The question since then has been: who’s next?

Zepto’s losses are down from ₹84 per order in FY24 to ₹59 today. But it’s still losing on every single transaction, with no parent company to absorb the pain.

Instamart has Swiggy. Flipkart Minutes has Walmart. Amazon Now has Amazon.

Zepto has VC money that must be returned. So why are retail investors still betting on it?

3 months of Wispr Flow free. Start today.

Wispr Flow makes writing quick and clear with seamless voice dictation. It is the fastest, smartest way to type with your voice. Our entire team has been obsessed with it since it launched. Try Wisprflow Pro for 3 months absolutely free by signing up using the link below.

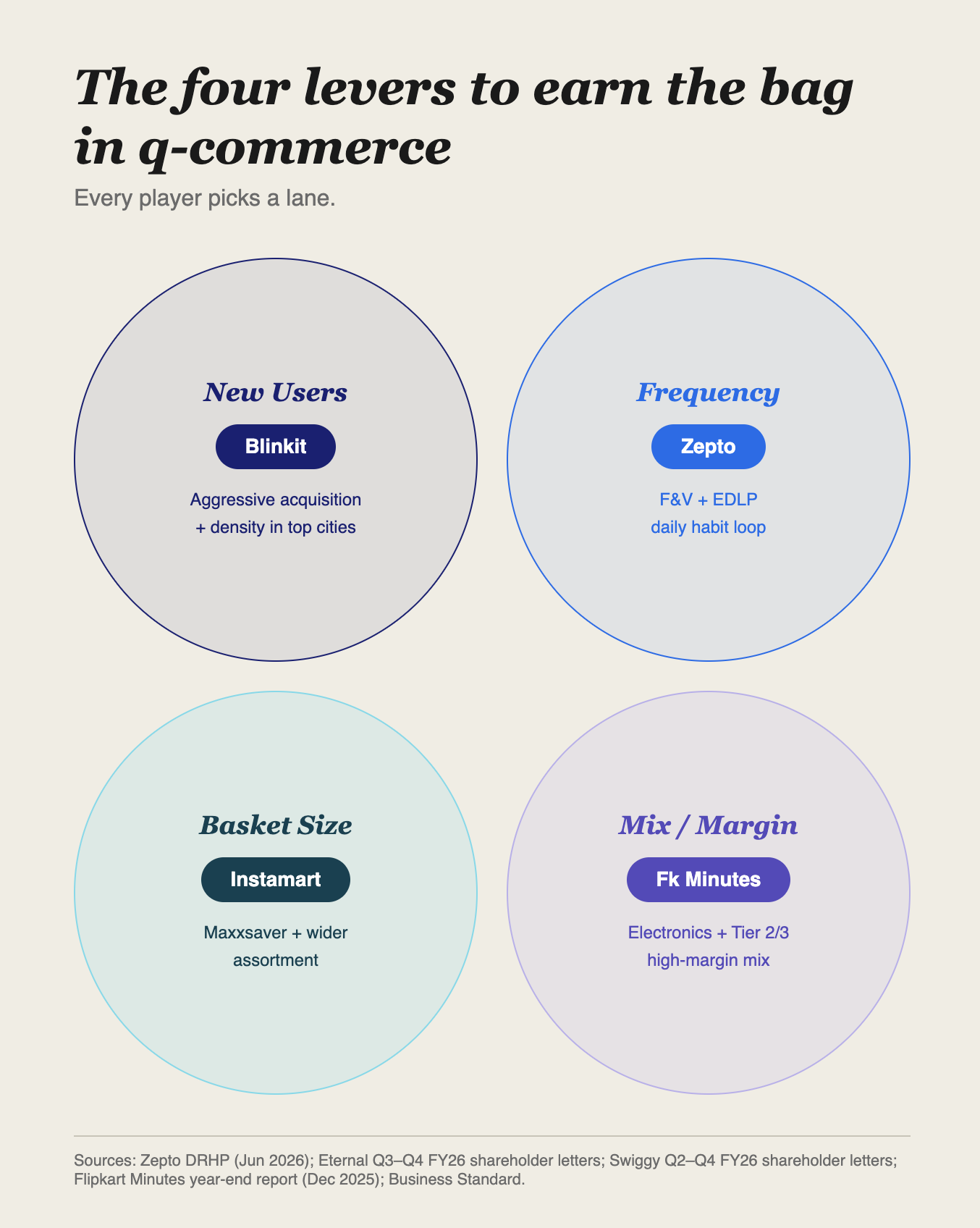

Zepto’s pulling a growth lever no one is.

Frequency. More people returning to the app = more sales = more commissions. Simple.

So, why aren’t more players doing it?

See, the items that bring users back have low margins. Vegetables, milk, curd, and rice have lower margins than electronics or beauty items, which are purchased only occasionally. Plus, customers expect discounts on q-commerce platforms today, making margins even thinner.

For perspective, on a ₹1,000 grocery order, platforms earn only ₹70-₹100 on average. That isn’t enough to cover delivery partner payouts, discounts & or even dark store costs.

This is precisely why platforms pursue other growth levers.

1. For Blinkit, it was new user acquisition.

Blinkit entered q-commerce with something no pure-play startup had: eight years of Grofers’ grocery supplier relationships, warehouse infrastructure, and a user base already trained to buy groceries online.

The rational lever for Blinkit was new users: get to density first, open more stores, and let operating leverage do the work.

After all, every additional order on a fixed store-cost base (dark stores, delivery agents, etc.) means a cheaper order to serve. More users also mean richer purchase data, which makes the advertising platform more valuable to brands and generates more ad revenue per order.

2. For Instamart, it’s largely basket size and Noice.

It didn’t have Blinkit’s supply chain and warehousing advantages. But they noticed that customers placed large orders. So, the basket size became the bet.

The logic is simple. Get the user to spend more per order. Use ads, if needed. And get commissions on a product mix (typically includes low and high-margin products), save on delivery, and earn ad revenue. That’s why Maxxsaver. Plus, higher margins on Noice (we covered Swiggy’s Noice strategy in detail here).

3. For Flipkart minutes, it’s high-margin electronics.

Why? Because it had direct partnerships with most electronics brands in India. Plus, each product could get high commissions. So, it used grocery as the filler, not the anchor.

So, why is Zepto still betting on frequency?

Q-commerce has a stickiness problem.

When the assortment looks similar, and every player promises 15-minute delivery, which platform should a customer choose?

Blinkit believes people will return to it for its reliability and breadth of selection. Instamart is betting on Noice. Zepto? Well, Zepto is betting predominantly on discounts.

Here’s the thing about discounts.

It’s expensive, and the platform almost always bears the cost. But in India, the customer follows the cost. Zepto’s hoping the behaviour allows retention with all-time discounting.

Behind Zepto’s discounting strategy.

It‘s called EDLP — Everyday Low Prices. Meaning permanent price reductions on categories that matter/ high frequency categories, like vegetables, milk, and staples. The kind that registers as “this is cheaper than the kirana store, Blinkit, and Instamart.”

What’s more, unlike a promotional discount that expires on Friday, Zepto can hold this price permanently because it owns the inventory and sets the price itself. A marketplace platform cannot make the same promise. The merchant does.

How will it bear costs? Advertising revenue from the brands whose products you’re buying for cheap.

Here’s how it works in practice.

Here's how it works in practice. A brand like Nestlé sells Maggi to Zepto at wholesale cost. Zepto discounts it 10-15% to the consumer. Nestlé accepts the lower margin because it gets volume and market visibility.

Then Nestlé pays Zepto again for the right to appear first when you search “noodles.” For a bundled deal that nudges you to add a second packet. For the data that tells Nestlé exactly which price point made you buy and which one made you scroll past.

That second payment is where Zepto makes its money back.

According to the DRHP, ad revenue went from ₹49 crore in FY24 to ₹1,635 crore in FY26. And ad receipts as a percentage of net retail value went from 1.11% to 7.78% in two years.

Long story short, discounting can bring people onto the platform and keep them there without breaking the bank. But what happens once they shop?

The supply side machine.

Zepto’s needs volume for the EDLP fulfilment math to work.

More orders per store means lower fixed cost per order. That means costs like dark store rent and delivery costs get split over a larger number of orders.

But opening dark stores takes capital, too. And with investor money quickly depleting, what is Zepto’s plan?

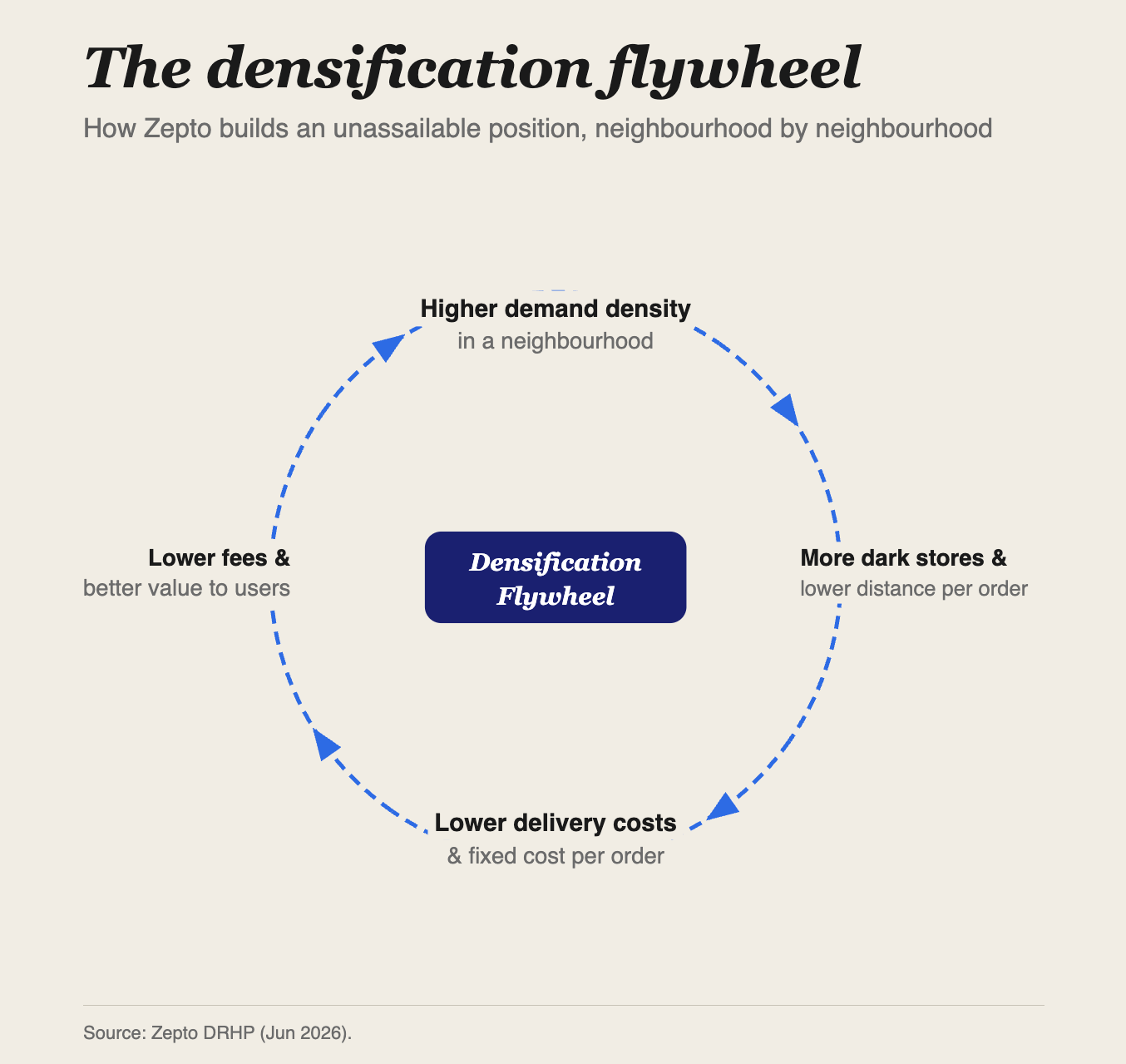

1. Area densification

Higher-order volumes in a neighbourhood justify opening another dark store there. More stores mean shorter delivery distance per order. A shorter distance means faster delivery and lower last-mile costs. Lower cost and faster delivery mean better user experience. Better user experience means more orders. More orders justify another store.

2. Franchisee dark stores

Densification requires capital. Every new dark store needs fit-outs, cold storage, racks, CCTV, and IT infrastructure. Per the DRHP, average capex per dark store runs approximately ₹7.94 million. At 1,904 stores planned from IPO proceeds alone, that is a significant capital commitment.

Zepto’s solution is the Growth Partners model. Third-party operators/franchisees set up and run dark stores under Zepto’s brand, using Zepto’s technology and delivery fleet. The franchisee bears the real estate cost and setup capex. Zepto perhaps pays them a commission. The franchisee owns the warehouse. Zepto owns the sale, the data, and the customer relationship.

The financial logic is precise. Zepto expands its physical footprint and order volume without a proportional increase in its own capital deployment.

Will Zepto’s survival strategy work?

The FY23 cohorts are the proof. Users acquired in 2023 stabilise at 45-50% retention through 12 to 15 quarters. They start buying across 2.6 product categories in their first month and expand to 18 by month 23. The habit forms. The economics follow.

The FY25 and FY26 cohorts are telling a different story.

The FY25 Q3 cohort's retention dropped to 31.1% by Q4. The FY26 Q1 cohort was at 32% by Q3. Both are materially worse than the FY23 cohorts were at the same stage. Whether they will eventually stabilise at 45-50% like the older cohorts remains unknown. That data will not exist for another 6 to 8 quarters.

It is a bet placed before the validation arrives, using public market capital to fund the gap between the proof and the bet.

Want to be scary good at AI?

Workflow guides got you started. But they won’t get you ahead. The founders, PMs, marketers, designers and engineers using Claude, Lovable and even Cursor — everyone who’s actually shipping — are inside GrowthX, building every weekend.

Build-focused events, expert-led sessions, AI credits, feedback, and community. It’s got everything except the excuse.

Want to plug your brand into our newsletter?

Email us at collab@growthx.club

Great insights