This phone brand shouldn't exist

How Nothing earned the right to exist in the hyper-competitive phone market.

Quick question before we start. How long does it take to type 100 words? About 2.5 minutes. Saying them out loud? Just about a minute.

That’s the idea behind Wispr Flow. Our team uses it every day — for Slack messages, creating scripts, crafting strategy docs, and even replying to emails. The best part? It makes 0 mistakes and nails the formatting every single time.

Sign up for GrowthX now and get 6 months of voice typing free.

Today’s edition.

There are two ways to disrupt the smartphone market: create a technology shift or ride a market one.

Apple cracked the tech. They brought the first mass-market touchscreen phone to a world that only knew keyboards. Samsung cemented its India position by riding the 4G wave harder and faster than anyone else. Both paths work. But both demand years of R&D and serious capital that a new brand simply doesn’t have.

So what’s left? Offer the most value-for-money phone. Except, 15+ Chinese brands with optimised supply chains are doing exactly that.

Legacy brands own consumer trust on one end. Aggressive Chinese players own the value end on the other. There is no obvious gap.

And yet, Nothing, founded in 2020, has managed to capture 2% of the Indian smartphone market. How did they do that? We tried finding answers to that question over the last few days. Here’s everything we learned.

The wedge is identity.

Carl Pei, the founder of Nothing, knew his new brand couldn’t compete on specs. Sourcing the latest and greatest components would be too expensive. Competing on price was out of the question too — no one wanted razor-thin margins.

Enter: tapping into identity through design.

It isn’t new. Apple did it back in 2008, when launching the MacBook Air, when Steve Jobs pulled a MacBook Air from a Manila envelope. The design of the Air was thin and sleek, unlike any other laptop, although it wasn’t entirely practical at the time. Everyone who bought it wanted to appear cool by association. Even at a premium price.

Nothing intends to follow the same playbook. But with a specific target: the back of the phone.

It’s where your identity lives. It’s what people see when you place it on a table, what they notice when you pull it out of your pocket — which is also why phone cases are a billion-dollar industry. But as build quality has improved across the board, every phone is starting to look the same.

That’s the gap Nothing wants to own. And here’s the practical upside — reinventing the back of the phone is significantly cheaper than competing on specs.

But locking a manufacturer is harder than you think.

Smartphone making is a volume business.

Think about it from a manufacturer’s POV.

A new phone company approaches you to manufacture custom components. You spend months figuring out the suppliers, the assembly, the entire production line. The numbers only work at scale — so you order big. The company launches, sells a few thousand units, then shuts down. Now, you have components for 100,000 phones and no one to sell them to.

Phone manufacturers know this story too well. It’s why they only work with partners who can guarantee volume.

Legacy brands like Apple get easy deals with Foxconn — there’s clear, persistent demand. Vivo, Oppo, iQOO, Poco, and Realme cut deals with Foxconn too, but not because of individual clout. They have one parent company, BKK Electronics, one negotiating table, and massive combined order volumes. For perspective, BKK Electronics controls roughly 45% of India’s smartphone market.

Nothing had neither the massive demand nor a large parent company to back it in 2020. No wonder Foxconn said no.

The first proof of concept: earphones.

No manufacturer wanted to make phones for a brand with zero existing demand. So Nothing went with earbuds, a lower-stakes product that required less capital, shorter production runs, and a smaller factory commitment. The kind of deal a struggling small manufacturer might actually say yes to.

The logic was simple.

If the earbuds sold, it proved two things — that consumers would pay for Nothing’s design language, and that the team could actually manufacture and deliver a product at scale. Proof of demand. Proof of execution. That kind of track record could open doors with bigger manufacturers.

The bet paid off. Nothing sold ~1,00,000 Nothing Ear (1) buds globally in the first 2 months of launch, signalling strong demand to other consumer electronics makers like BYD China. The company went on to become Nothing’s manufacturer for the Nothing Phone 1.

Finding the right pricing market fit.

But where do you even position yourself? Flagship, mid-premium, or budget. Each caters to a different customer who wants fundamentally different things. And the size of each group keeps shifting.

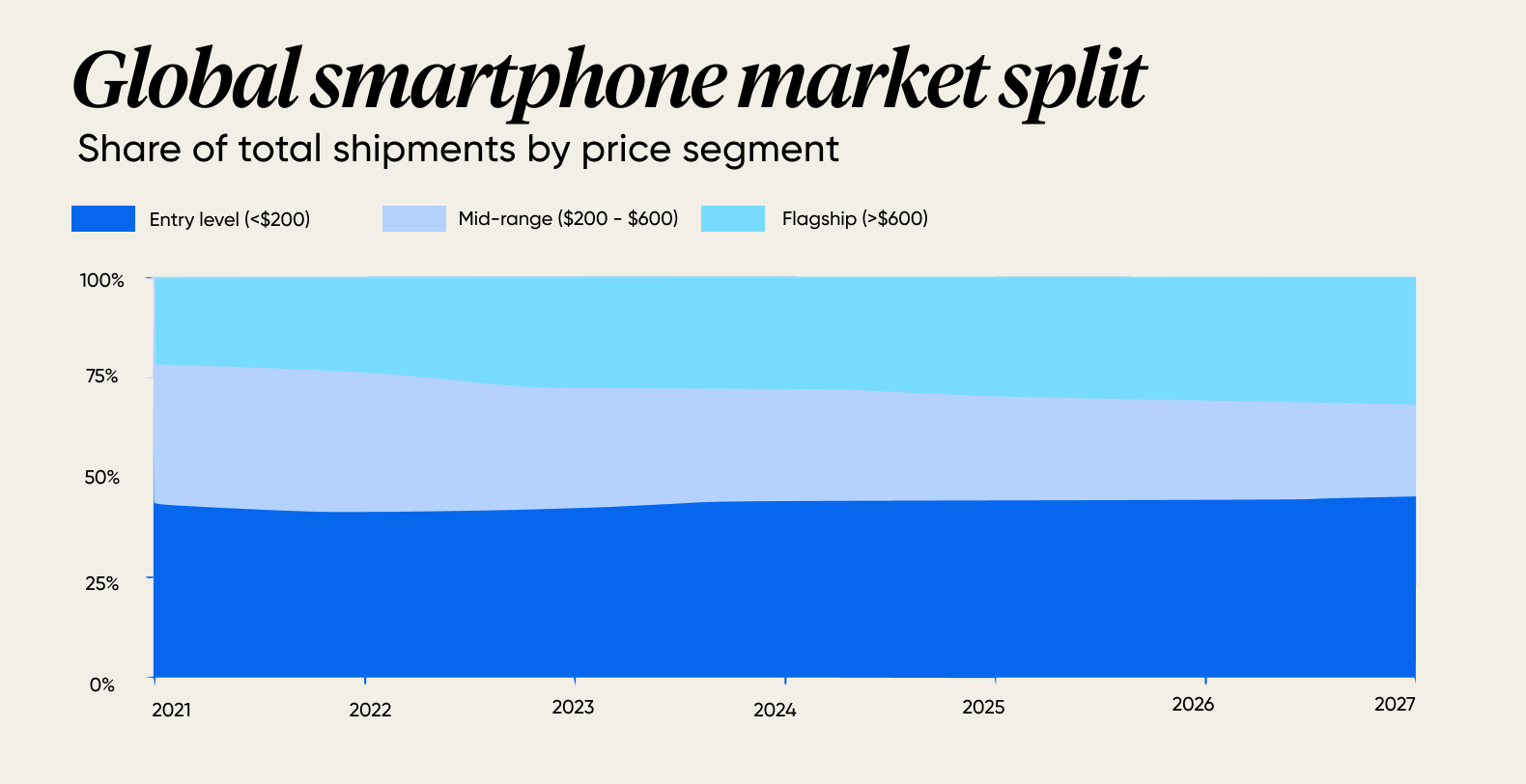

Take a look at the chart below.

In 2022, entering the mid-range segment was the obvious choice.

This way, Nothing could avoid the volume game of budget devices, while having just enough specifications to cut through the competition and make a margin. Brand loyalty was weak here too — every player was focused on specs, not design. Which meant Nothing had a real differentiator on its hands, provided it could crack the right design-spec-price configuration.

Nothing Phone (1) launched in 2022 at ₹32,999 in the mid-range segment, in the same segment where OnePlus built it name.

Around 2023, the market shifted.

By 2023, the market was shifting. No-cost EMIs made premium phones more accessible, build quality improved, and replacement cycles got longer. Customers started trading up. Many competitors went up-market. But Nothing took the opposite route.

The Nothing Phone (2) went for ₹45,000 in 2023, featuring a better chipset, a premium build, and improved cameras. The Phone (2a) brought the same experience down to ₹24,000. The Phone (2a) sold 60,000 units in the first 60 minutes.

The lesson?

Stay anchored in mid-premium to build credibility, because no one buys a flagship from a brand they don’t trust yet. Move downmarket simultaneously to capture volume. Two reasons.

One, because ~50% of the Indian population is looking for a budget phone. And two, because scale gives you leverage with suppliers, manufacturers, and retailers and raises sales with customers.

And so, in 2023, Carl introduced the CMF lineup of consumer electronics.

Wait, why start a new brand?

Look at it from a customer’s perspective. You’ve been saving up to buy a mid-range phone for some time. Would you rather get a Pixel 9a or a Xiaomi 14 Civi? Unless you’re a Xiaomi fan, it’s probably the Pixel 9A. Because of its association with Google.

Customers trade up toward brands they trust, not down. And by 2023, Nothing had already built a reputation as a design-first, mid-premium brand. That credibility was worth protecting, which is exactly why they didn’t put the budget phone under the Nothing name.

In 2024, Carl launched the first phone in the CMF lineup — the CMF Phone 1 — at ₹ 16,000.

Misdirection and course correction.

In 2025, Nothing tested the premium segment. Three years in, with a loyal customer base — was there appetite for a flagship? The Nothing Phone (3) launched at ₹80,000. Signature dot-matrix design, superior build quality, but a mid-tier Snapdragon chip. At that price point, customers compare every rupee against what Apple and Samsung are offering. The chip was an easy target. Sales were modest.

The Nothing Phone (4a) came back to the ₹34,000 price point. First week sales exceeded internal targets by 150%. You had to earn the right to enter the premium segment; you couldn’t bulldoze your way in.

What’s next for Nothing?

Carl Pei wants Nothing to be a top-five global smartphone brand within a decade. That means going up against Apple, Samsung, Xiaomi, vivo, and OPPO — companies that ship 150 to 250 million phones a year. It’s an extraordinarily ambitious goal.

But Nothing has already survived the phase where most startups don’t make it. The harder question now is whether they can grow from a cult brand into a mainstream one, without losing what made them worth following in the first place.

Lovely read!