Reality behind BlinkIt's $13B game 🛵

How is Blinkit dominating India's quick commerce space?

The Blinkit magic✨

Zomato acquired Blinkit in 2022 to enter the quick-commerce space but little did anyone know that this “grocery-delivering” business would become more valuable than Zomato’s own food delivery business. Yes, you heard that right! Btw, Blinkit is also leading India’s quick commerce game with a 46% market share and a $13 billion valuation (given by Goldman Sachs). Let’s dig in..

But, how does this dhandha work?

To decode the unit economics, we read multiple reports — ones by JM Financial, Citi & JP Morgan. So here we go, to calculate this, assume the average order value (AOV) of ₹600, which is pretty close to the company’s real AOV of ₹650. Now, break this down into the revenue side (a.k.a “Take Rate”) and the cost side.

On the cost side — you have line items like last mile & mid mile delivery, dark stores & warehousing, packaging, customer support, and multiple customer acquisition costs like the “20% discounts” to lure you.

On the revenue side — you have line items like warehousing & marketplace commissions (earned from suppliers), ad income (earned from brands), and delivery charges (earned from customers).

We have done the calculation for both below👇

The difference between the two amounts (₹110 - ₹94.8) i.e. ~₹15 is Blinkit’s contribution profit. Yes, not “net profit”, because it doesn’t include fixed expenses like office rent, assets, insurance, depreciation, and many more. Contribution margin is an industry metric used by players to measure how each transaction on the platform contributes to the overall company profit.

Contribution Profit = Price per unit - Variable cost per unit. Btw, Blinkit is contribution profit positive, each sale is adding to Zomato’s overall profits.

What did Blinkit crack then?

Bigger scale game.

But, how does Blinkit ensure that all customers in the city get their orders? And not just that, how does it ensure that customers get the orders within 15-20 minutes? The answer is *drum rolls* Dark Stores – the 2.5k to 4k sq. ft. stores located within a radius of 1.5-3km of our homes. One dark store can have up to 6,000 SKUs - 4X of your nearest Kirana Shop. Fun fact: For every ~40 dark stores within the city, there’s one 10X bigger mother warehouse on the outskirts (20k to 175k sq. ft. big).

Blinkit has the highest number of dark stores compared to its peers. Plus, it has done a killer execution as a dark store’s location decision involves taking in factors like—

Average household income

Infrastructure & peak traffic

Population density

Higher AOV game.

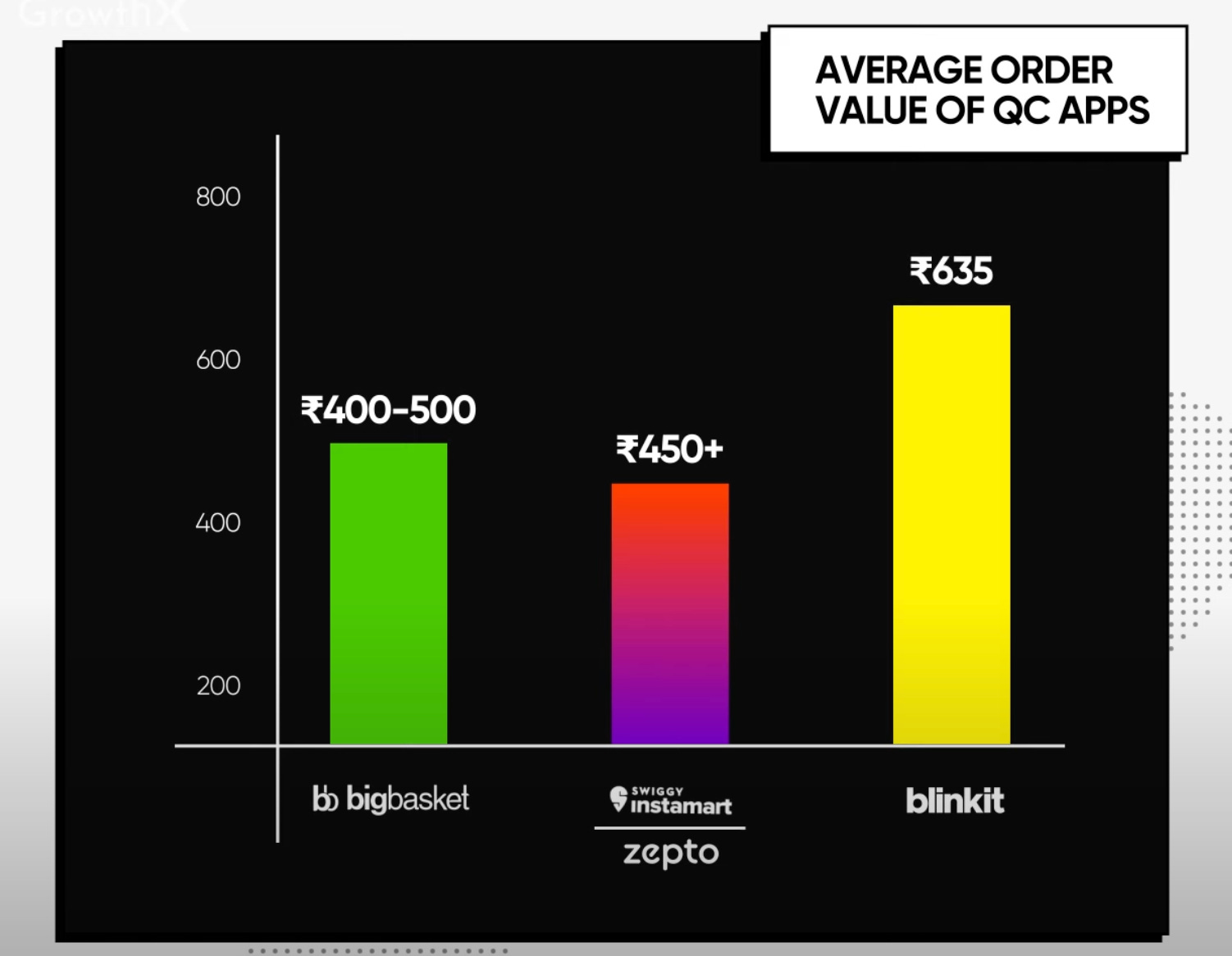

Scale is just one part of the puzzle — Dark stores don’t get you high average order values. But why are AOVs important? Look, a higher AOV means a bigger chunk of contribution profit from the same customer. It also means higher ROI with same effort & cost of delivering the order. But this is easier said than done. BlinkIt’s AOV of ₹650 is way higher compared to competitors who are stuck at ₹400 to ₹500 range. The secret sauce is in the app’s positioning.

While everyone is getting creative by adding more “Amazon-like” options on the app, Blinkit has played with customers’ psychology with their super bold initiatives like getting an iPhone or PS5 in 10 minutes. The idea is simple: Create buzz → Position as a “One Stop” marketplace → Get more customers + Get current customers to order more.

The Zomato effect.

Blinkits’ market share has not been the highest forever. It was 32% in 2022. And in this same period, Instamart’s share fell from 52% and Zepto’s increased from 15% to 28%. But one unfair advantage lies in the parent company.

See, Zomato is the biggest food delivery app with a 56% market share and 100M+ monthly active users — 3X what Blinkit has. So even getting 5% of Zomato’s monthly active users as new customers, could bring more 33% rise to the app’s current MAU base. Zomato has done an integration at the bottom of the app so that users can access Blinkit within a blink. Zomato has deliberately kept the 2 apps different because the company knows that super brands > super apps in India. So, there’s no point leaving the brand effect Blinkit has created in 10 years.

That’s not all, we launched a new episode of GrowthX Wireframe, where we cover Blinkit’s business in depth —

Thanks for supporting this newsletter

If you’ve enjoyed this piece, do consider referring our newsletter to a friend. For your first referral, we’ll send you our Infographics ebook, which has a collection of growth & business infographics that have generated 1 Million + impressions on socials.

Great read!

To ensure profitability & CMs sticks around, an operational heavy company like ‘Blinkit’ necessarily has to take the route of establishing in areas of high demand and capturing the low hanging fruits first.

Reminds me about an article over BluSmart’s business model and how their routes are firstly optimised wrt the high demand use cases, airport travel, key office travel (in BLR)