Nike has a huge conversion problem.

It's costing them their ₹1380 Cr market.

Most voice agents die in the demo room. Cost, latency, and memory — fix one, the other two break. Fixing all three in a day sounds like a fever dream.

Up for the challenge? ElevenLabs covers the credits. You pick your brain — OpenAI, Claude, or Gemini. We handle the room.

Today’s edition.

Every brand’s marketing budget exists to achieve top-of-mind awareness (TOMA). The premise is straightforward: the brand a consumer thinks of first is the brand they buy.

Nike has it. In India, when someone says sneakers, the answer is almost always Nike. And yet, Nike (~₹1200 Cr) ranks third in revenue among the big three, behind Puma (~₹3274 Cr) and Adidas (~₹3114 Cr).

Why is that? To understand it, let’s look at the playbook most sneaker brands follow.

India’s sneaker market playbook.

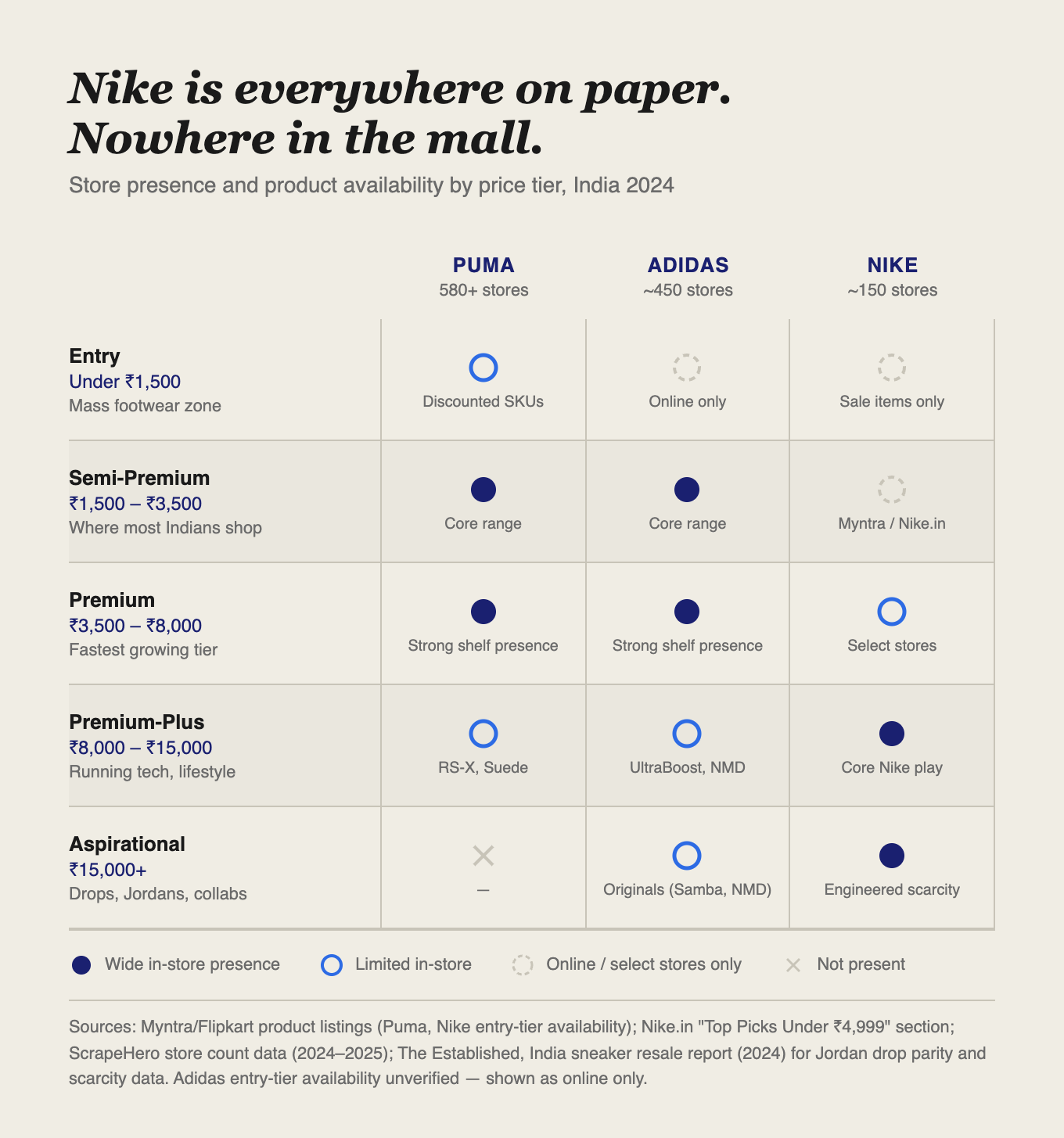

Cracking India as a sneaker brand follows a reliable formula. Get into as many malls as possible. Sign a Bollywood star or a cricketer. Price competitively — the Indian consumer is value-conscious, and a ₹3,000 shoe will always outsell a ₹8,000 one. Build India-specific campaigns. And most importantly, show up where the customer is.

Puma followed this to the T. 570 stores. Kareena Kapoor. India-designed products. A price range that starts where most Indian wallets are comfortable. The result is in the revenue numbers. Same with Adidas.

Now compare that with Nike. Just 150 stores. No cricketer on contract. No mall saturation. Even the campaigns it has run in India are cultural bets, not sales plays. By every conventional measure of what it takes to win the Indian market, Nike is doing it wrong.

So, why is it still relevant?

The science of premiumization.

It’s actually a cultural play for Nike.

Back in the 1980s, Michael Jordan signed a shoe deal with Nike. The Air Jordan 1, didn’t sell because it was a good shoe — it became the object through which an entire culture expressed itself. Basketball, hip-hop, and street style fused around it.

That culture took decades to reach India. It didn’t come through advertising. It came through NRI relatives returning with pairs that weren’t available here, through pirated NBA highlight tapes, through the internet, and eventually through Instagram.

Then, Ye collaborated with Adidas to create the Yeezy, and for the first time, Indian consumers had access to the most coveted silhouettes in lifestyle sneakers. The pairs were extremely limited. They sold for ten times their retail value in the aftermarket. It became something to brag about.

Nike rode directly into this current. Retro Jordan drops followed. India’s resale platforms — VegNonVeg, Crepdog Crew, Superkicks — built their entire businesses around the drop calendar. By the early 2020s, India was receiving nearly the same Jordan drops as the United States.

Over time, Nike became the brand everyone wanted to have a slice of. Then, it built three engines to make sure the feeling never left.

1. Athlete association.

Not local ambassadors hired to hold a product at a photo shoot, but global figures whose entire careers are woven into the product itself. The Air Jordan 12 “Flu Game” exists because Jordan wore it through a 38-point performance while visibly ill in the 1997 NBA Finals. The colourway is a timestamp. When Nike releases 500 pairs of a specific Jordan colourway, they’re releasing access to a documented moment in cultural history, with a fixed supply and a growing number of people who want it.

2. Scarcity.

A Jordan 1 drop releases 500 pairs. A hundred thousand people want them. The 99,500 who don’t get one don’t forget — they follow the resale listings, tell people about the shoe they almost got, and come back for the next drop.

When an Air Jordan x Off-White Chicago retails at ₹19,000 and resurfaces on Crepdog Crew at ₹4,25,000, Nike doesn’t pay for that signal. The resale market broadcasts it for free, to exactly the audience that cares most.

3. Store experience.

You don’t walk into a Nike flagship to browse. You walk in having already decided. The store exists to confirm a desire that formed elsewhere — on a resale listing, on a drop that sold out before you could refresh the page.

It all rides on sustained hype.

What happens to Nike when the hype dies?

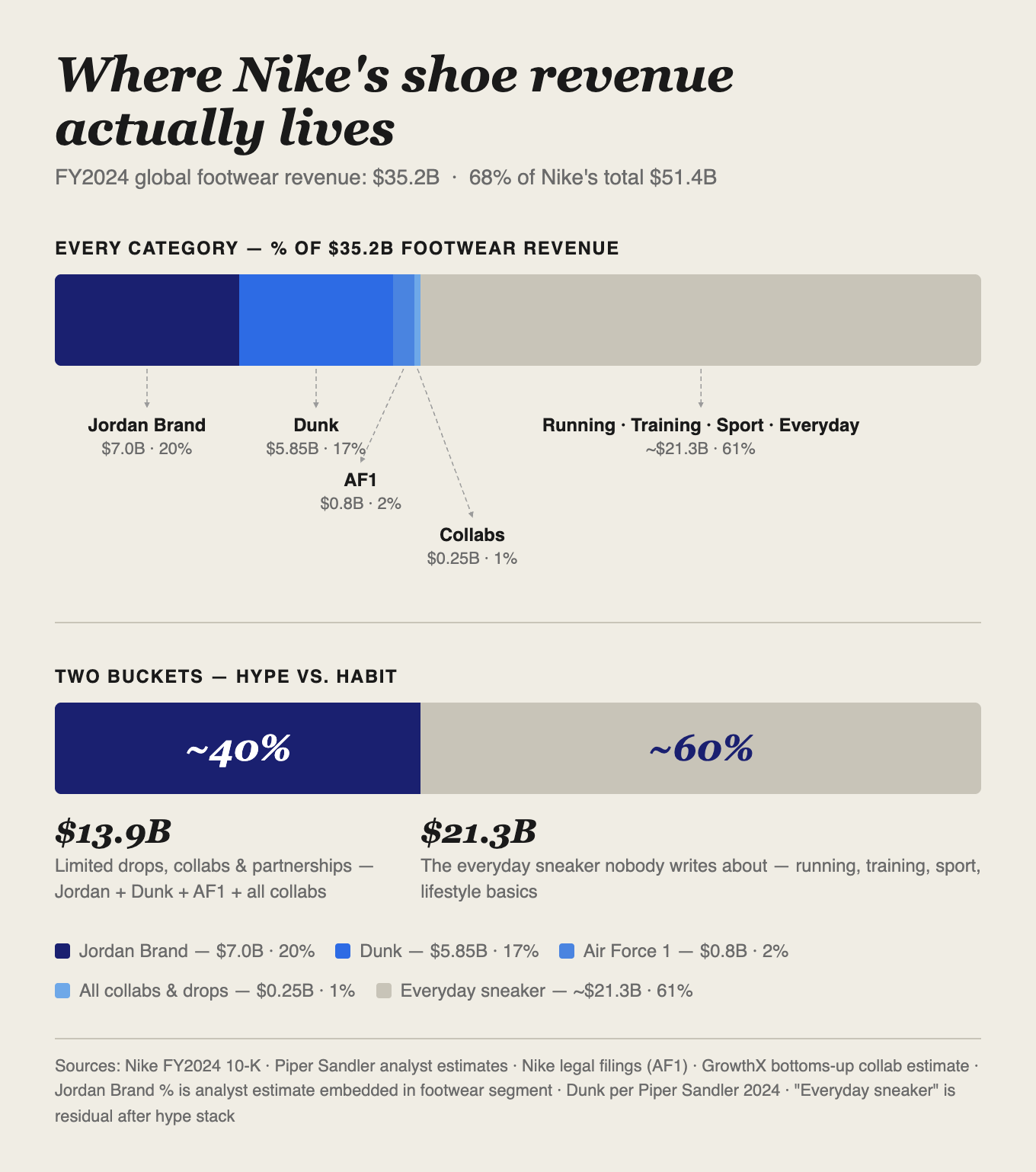

Hype accounts for aout 39% of Nike’s revenue (2024). The rest comes from daily wear shoes and sneakers.

That part of the business grows the way any consumer product grows: through distribution reach, product quality, and the trust that a brand accumulates over time.

Nike's relationship with the Indian consumer has moved through three distinct phases:

1. The Swoosh collab with the Indian Cricket Team

From 2005 to 2020, the Swoosh sat on the Indian jersey through World Cups and bilateral series — fifteen years of the most-watched sport in the country. It made Nike visible, but not trusted.

2. Da Da Ding Campaign

The women-facing campaign featured hockey player Rani Rampal, cricketer Harmanpreet Kaur, surfer Ishita Malaviya, and eight other Indian sportswomen alongside Deepika Padukone — a former national-level badminton player herself. That brought 2.8 million YouTube views in the first week.

Nike understood was that professional athletes are a trust signal that celebrity ambassadors cannot replicate.

3. Nike Run Club

Focused around the country’s running culture, this club operates across Bengaluru, Delhi, Mumbai — free coaching, pacing sessions, structured runs open to anyone who identifies as a runner. This way, the brand that owns the habit owns the revenue that actually funds the operation.

Positioning themselves as premium and maximising brand visibility through marketing can create pull for Nike. But that alone cannot solve for distribution.

Nike’s distribution problem.

The brand that built three decades of cultural pull — through Jordan drops, Da Da Ding, Nike Run Club, and the steady accumulation of global aspiration — ran its India operation on ~100 stores. Anyone who wanted to buy Nike but didn’t live near one of those stores had one other option: buy online.

Why didn’t Nike didn’t invest in offline retail

It all started in 1995, when Nike entered India through a single licensing partner — SSIPL — and grew its retail presence only as fast as one franchisee could fund and operate stores. By 2002, Nike had 25 exclusive outlets across India, a number that bloomed to ~350 by 2015.

That said, the stores were loss-making since 2006.

See, globally, Nike created mono-brand outlets ~25% of the time, with the rest of the distribution handled through multi-brand sports chains. Multi-brand sports chains didn’t exist in India in the early 2000s. So, Nike pivoted to mono-brand outlets simply because it could control the entire display and in-store experience and manage inventory turns.

But retail economics broke down.

A mono-brand Nike store in a premium Indian mall requires 1,000–1,500 sq ft. At ₹200 per sq ft minimum guarantee — the standard mall leasing structure in India — that’s ₹2–3 lakh per month in rent before a single pair is sold.

Nike’s Indian stores were operated by its licensing partner SSIPL, not Nike directly. SSIPL bought inventory from Nike at wholesale and sold it at retail — keeping roughly 35% margin on each pair. On a ₹10,000 shoe, that’s ₹3,500 to cover rent, staff, and operating costs before profit.

Meanwhile, a Puma franchisee in a Tier 2 city needs to sell roughly 150 pairs a month at ₹4,000 to cover costs. Enough people in that city can afford ₹4,000. A Nike franchisee in the same city needs to sell 60–90 pairs at ₹10,000. The number of people in that city who will walk into a dedicated Nike store and spend ₹10,000 on a shoe — without an event, a drop, or a specific reason to be there — is simply smaller.

Online retail emerged much later.

In 2011, Nike’s India management decided to never let online revenue cross 5% of total. It was an attempt at protecting of the brand’s gilded image at the cost of the brand’s reach.

At the same time, Puma went to 50% online. The consumer who had been primed by fifteen years of cultural build-up who knew the Jordan, followed the drops, ran with NRC on Saturday mornings — finally decided to buy, opened Nike.in, and hit a wall. Payments failed. Refunds took months. Sizes were inconsistent. The experience that Nike had refused to build online was no better than the experience it had refused to build offline.

In February 2026, Nike handed Nike.com India operations to Nykaa — faster deliveries, simpler returns, curated inventory. Nineteen years after the distribution problem became visible, Nike found a solution. But by then, Hoka, On Running, and New Balance had already built their own aspirational positioning in the shelf space Nike had spent two decades leaving empty.

Nike’s market is compressing.

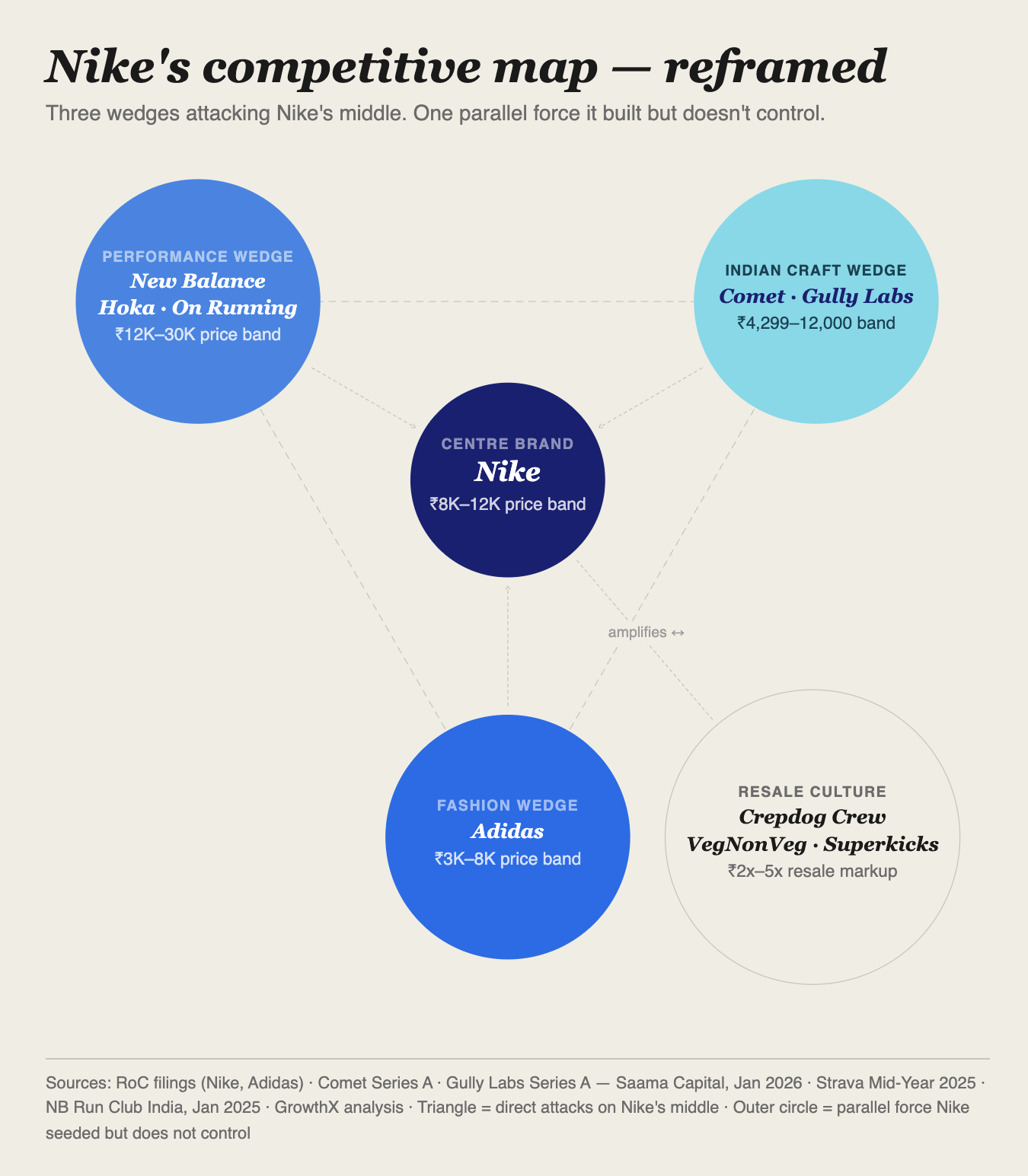

Adidas is bullying Nike into oblivion.

Adidas has surrounded Nike on every side. Need a budget shoe? Adidas has a Nike alternative at a lower price. Want a fitness sneaker for pilates? UltraBoost, ₹15,000–18,000. Want a fashion sneaker? The Sambas are sitting right there at ₹10,999.

Adidas moved deliberately from the fitness sneaker market — growing at 5.15% CAGR — into the fashion sneaker market, growing at 5.45% CAGR. Two separate product lines, two separate consumers, two separate store formats. The Originals stores don’t stock UltraBoost. The performance stores don’t sell Sambas. Adidas speaks clearly to each consumer without confusing either.

And then it put those products everywhere. Adidas eliminated the one-to-two month lag between global launches and India launches — the gap that had been losing it the well-travelled Indian consumer. Whoever wanted a ₹10,000 shoe walked into a mall and found Adidas four times more often than Nike.

Homegrown brands are redefining culture and identity.

Nike spent thirty years teaching Indians that a shoe could be an identity statement. Brands like Comet and Gully Labs are redefining what it means in 2026.

Comet priced its first sneaker at ₹4,299 — above the domestic budget brands, below the global premium tier, in exactly the gap Nike’s distribution strategy left open. The drops sell out in fifteen minutes to two hours.

Gully Labs operates one tier higher. Sneakers priced between ₹5,000 and ₹15,000 — Nike’s price band, not below it. Handcrafted in Delhi using Phulkari embroidery, Onam-inspired silhouettes, and regional craft traditions stitched directly into the product.

This is the threat Nike didn’t model for. Adidas can be countered with better drops and more stores. The Indian craft wedge cannot be countered at all — Nike will never make a Phulkari sneaker that feels authentic.

The new runner’s shoe.

Nike launched the first run club in India — starting in Mumbai and Bengaluru, expanding to Delhi in 2014 — six years before running became the urban professional’s identity sport. Free training plans. Pace groups. Gait analysis. Expert coaches at Nehru Park at 6 am every weekend. The runner who started in 2012 wore Nike.

That early presence created something more valuable than market share. A loyal runner buys two to three pairs a year without comparison shopping. They recruit their pace group. Customer acquisition cost effectively drops to zero because the runner handles marketing. And running shoe loyalty is stickier than fashion loyalty — when someone finds a shoe that works, they don’t experiment.

When loyalty fractures, the economics reverse.

And that fracture is happening for Nike. At Mumbai Marathon 2025, ASICS was the most-worn brand among full and half-marathon runners, commanding over 28% and nearly 30% respectively. Nike followed at around 20–22%. Globally, Strava’s 2025 Year in Sport data placed ASICS as the most-logged brand with 27% of gear entries. The Hoka Clifton ranked third, appearing in 18% of all logged runs — a brand with no official retail presence in India.

What’s next for Nike?

Nike is in the middle of brand management’s biggest dilemma — how do you become memorable without becoming ordinary? The brands that occupied the space Nike left open built loyalty there precisely because the space was empty. Move in aggressively, and Nike risks softening the only asset that has kept it culturally dominant despite sitting third on revenue. Stay back and the gap compounds — in stores, in runner loyalty, in the first-time buyer who never enters the funnel.

There is no good option. So, what will Nike really do? We’ll keep watch and report to you.

Well explained, I noticed something unusual in the writings is that

There are spelling mistakes one or two

Is that intentional just to prove it's not AI?