Maggi's competitors are here.

200+ brands want a share of instant noodle's ~₹13,000+ Cr. market.

Before we begin.

Last weekend, 33 non-coders shipped one product each. It took 4 days and not even a single line of code. The only support? Tools, frameworks, and real-time feedback.

We’re putting together the next room soon. Want in?

Today’s edition.

If you’ve taken a business course, you know that large product categories fragment easily. Take chips, for instance.

A ₹14,000 Cr. market with Lays alone holding 30%. Players like Bingo compete on flavour, while Balaji and other regional players compete on availability and price.

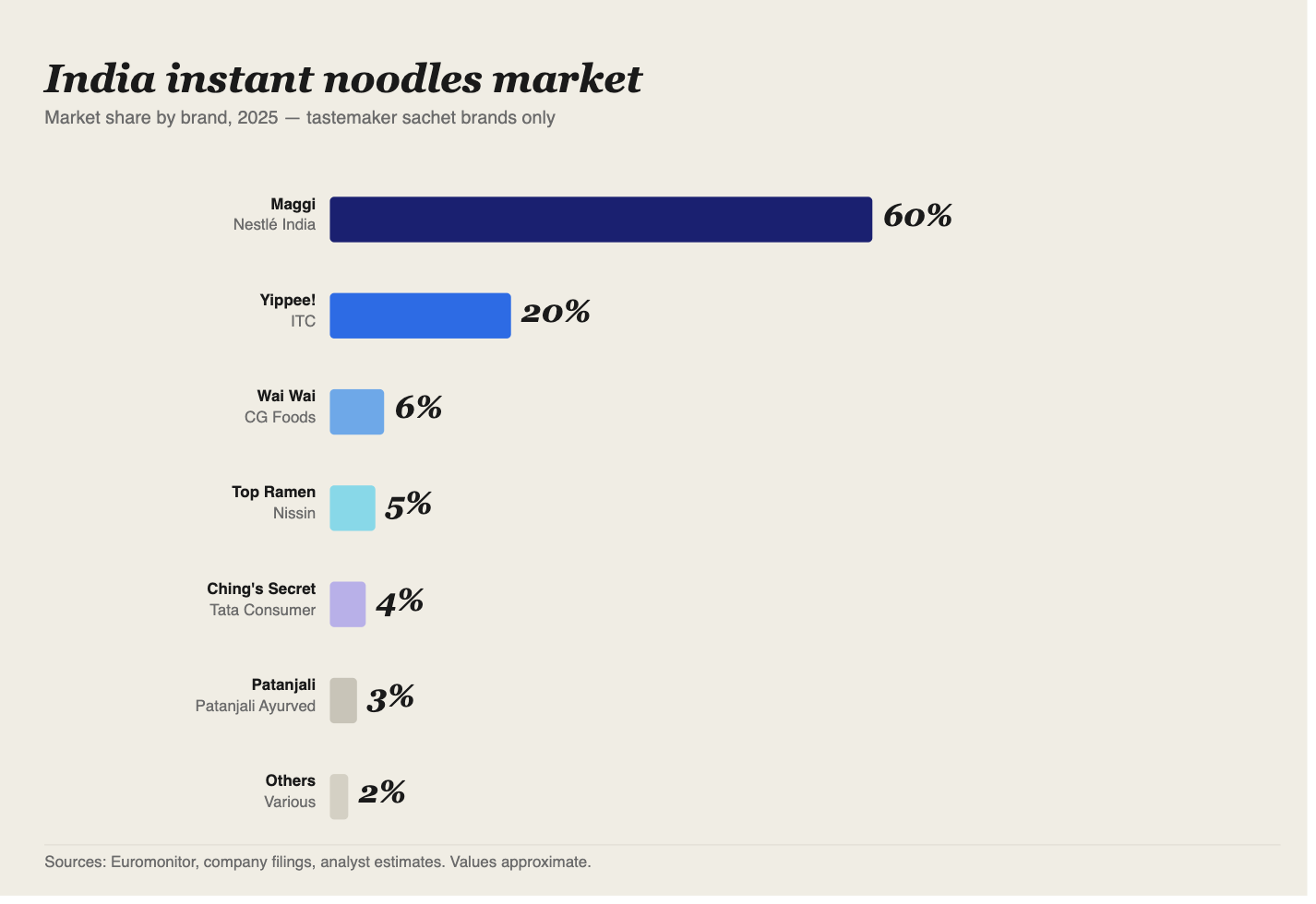

Now, look at the instant noodle market. Worth ₹13,000 Cr., but the market segmentation? Hugely different. One player, Maggi, holds 60% of the total share. That, too, with a core product that hasn’t changed in ~40 years.

Before we get into the competition, let’s take a good look at why Maggi continues to maintain its position.

Behind Maggi’s unbreakable moat.

Nestlé launched Maggi in 1983. The idea was to offer a mealtime option for households pressed for time. One problem. No one ate noodles for meals.

Indian kitchens were built around rotis and sabzi in the north and rice and curries in the south. It was a hardwired habit in adults, one that advertising alone couldn’t change.

Only one target group seemed to care about Nestlé’s new snack option. Children.

Separating the customer from the consumer.

Here’s the thing about children. It’s easier to sell to them. Price isn’t a factor, and a good product experience is enough to lock them in. The problem? They aren’t the end buyers.

But children can influence them.

The formula then is this. Appeal to the adult planning the meals — the mother.

That means hitting three things at once: nutrition, taste, and preparation time. Add free samples at school to the mix, and you have an easy trial-and-repeat loop.

Cementing presence across economic levels.

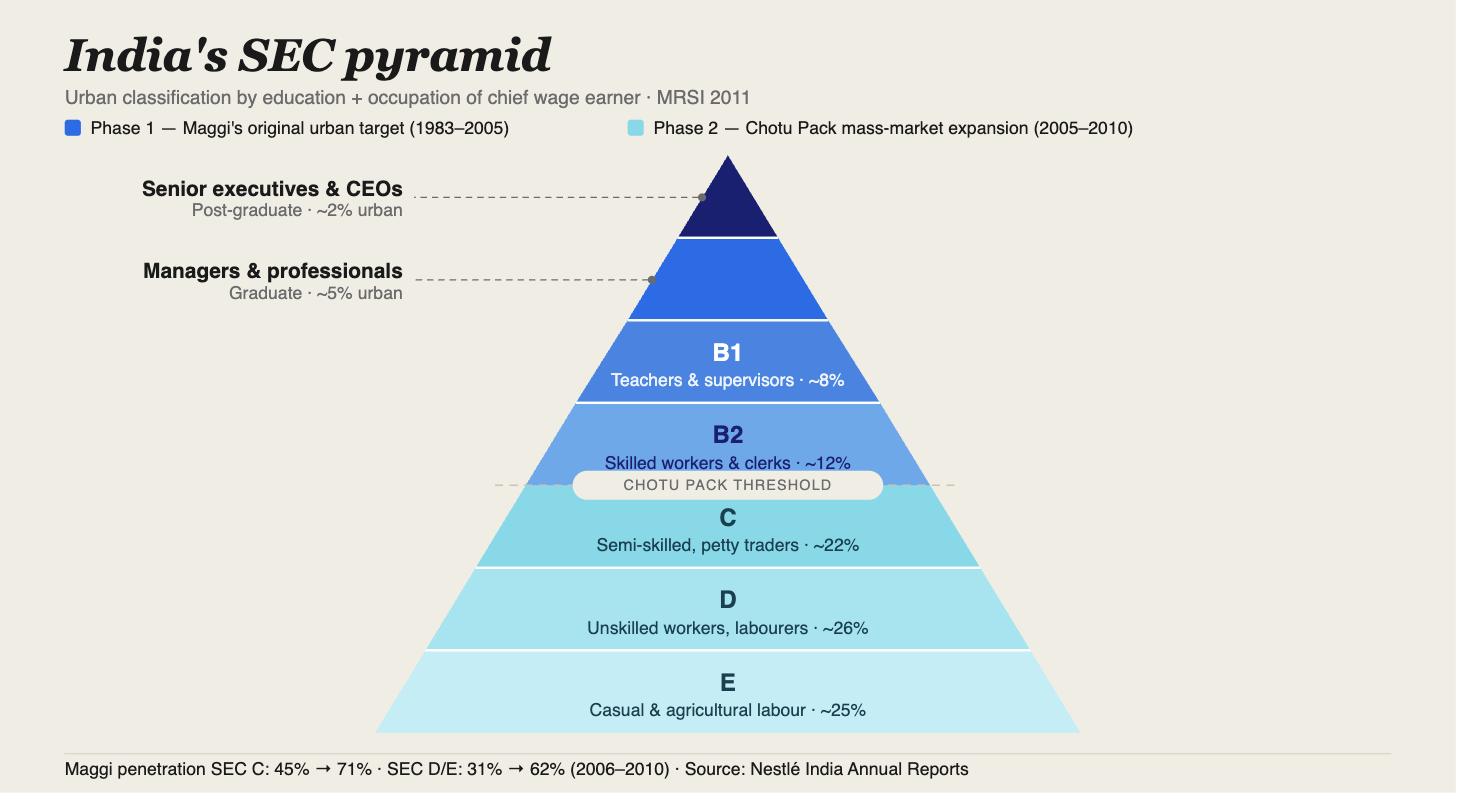

The indian customer isn’t a monolith. According to the Market Research Society of India (MRSI), based on Socio-Economic Classification (SEC), it’s segmented into 5 different categories — each with a different income level, and therefore with different product expectations.

By the mid-2000s, Maggi was the Number 1 Most Valuable FMCG Brand in India by NCAER. A dominant position — except for one thing. SEC A and B combined represent just 28% of India’s population. But the urban playbook that worked so well was the wrong playbook for a household where ₹5 is a real price consideration.

Maggi’s semi-urban expansion playbook.

Nestlé ran two go-to-market strategies simultaneously under the same brand. For price-sensitive markets, the Chotu Pack at ₹5 — not just a smaller size, but a market entry vehicle that expanded Maggi’s reach by 300,000 new outlets in a single year.

For rural and semi-urban markets where basic nutrition mattered more than taste, Maggi Rasile Chow — a low-cost, iron-fortified meal developed specifically for that consumer. Vernacular advertising in local languages for local markets. And underneath all of it, a distribution infrastructure built from scratch for places a truck has no business going.

Behind Maggi’s rural distribution layer.

Think about it. A distributor’s truck operational cost is ~₹8,000–12,000 a day. In a city, one stop at a large retailer yields an order of ₹20,000+ — the economics work. Compare that to a small town where the average retailer's order value is ₹300 worth — the economics break down.

Every major retailer in India solves this with the hub-and-spoke sub-stockist model. A local operator buys a larger consolidated order from the main distributor, then redistributes in small quantities to 30–40 nearby retailers within a 10km radius using a motorcycle or cycle rickshaw. The vehicle cost is negligible, and the aggregation makes the economics work. But logistics is one part of the problem. The other is how rural retailers operate entirely.

Rural retailers operate almost entirely on credit. They pay for the stock after it is sold. It makes sense for a stockist to know who to sell to. And that’s knowledge isn’t just hyperlocal; it only builds over time.

If that’s not enough, there’s the logistics rhythm — which roads flood in monsoon, which day the weekly haat runs, how much stock moves in summer versus winter. An established Nestlé sub-stockist had all of this dialled in. A new Yippee distributor in 2010 would have had to learn it from scratch, absorbing the bad debt and the wrong bets along the way.

And because distributors in Indian FMCG are exclusive to a single manufacturer, every stockist already signed with Nestlé was simply unavailable.

Brand affinity through availability

Once Maggi was physically present at the highway dhaba, the hill station shop, the district college canteen — it became the default answer to hunger in places where nothing else existed.

Availability created familiarity. Familiarity became habit. Habit became occasion. Every occasion you associate with Maggi is because Maggi has found a way to be present every time those moments happen.

Now, take a look at the distribution of the instant noodles market — doesn’t Maggi’s share make sense?

How to topple the instant noodle giant?

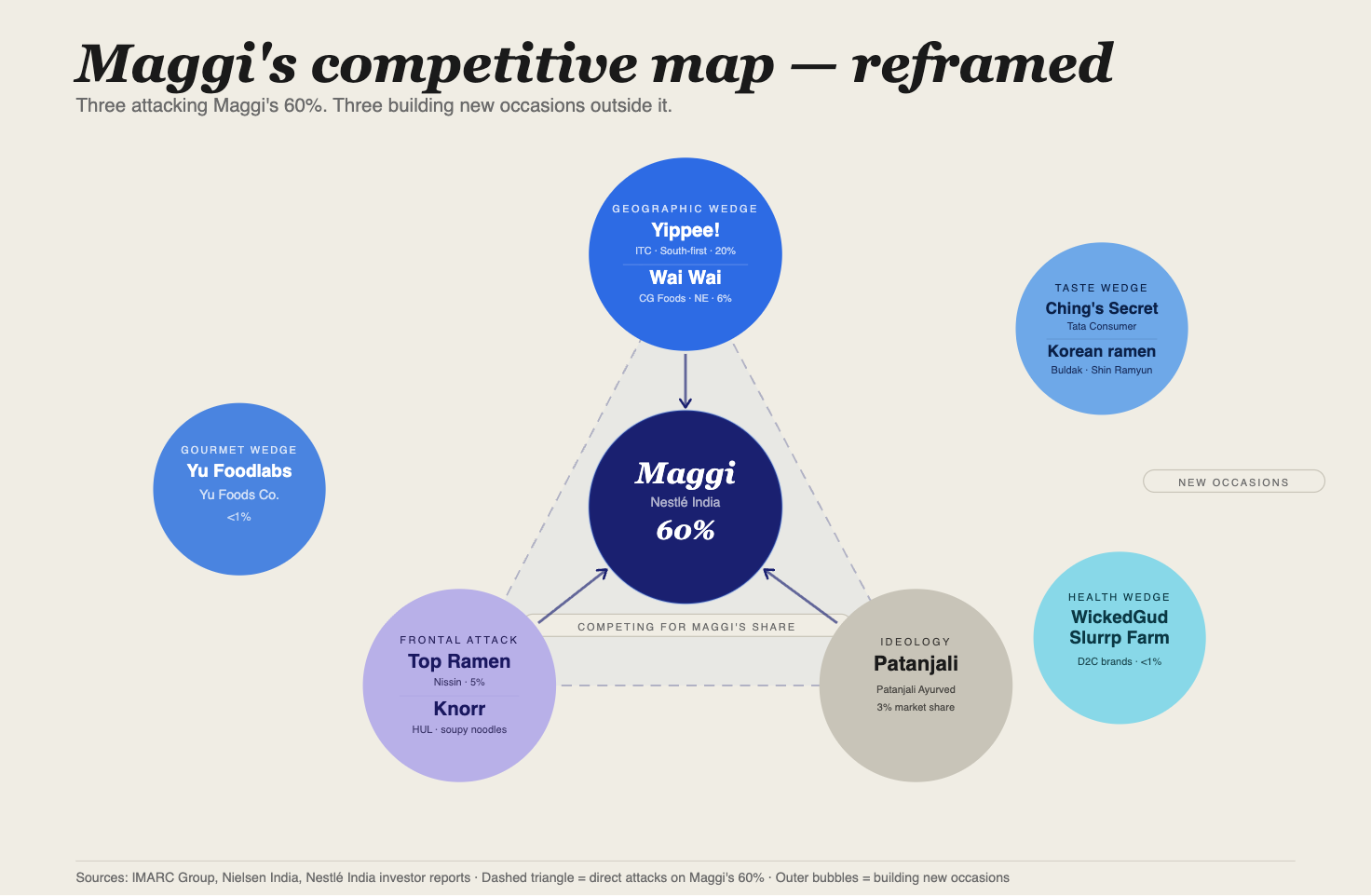

Maggi incumbents use several tactics. Let’s look at them one by one.

1. Frontal attack

Here’s a question worth sitting with. Nissin invented instant noodles. HUL has the deepest distribution network in India. Between them, they’ve spent decades and crores trying to crack Maggi’s market. Combined share today? Under 6%.

What went wrong?

Top Ramen entered in 1991 with a soupy noodle product — the format that works everywhere else in Asia. The packets didn’t move. So they relaunched in 1992 as a dry masala snack, copying Maggi’s format almost exactly. Same occasion, same consumer, same price point. Across 3 lakh retail outlets.

Maggi’s share didn’t have a dent. Because Maggi had 20 lakh.

HUL understood the distribution problem. In 2010, they threw 9 million retail outlets and Kajol at it. Knorr Soupy Noodles launched across South India, its strongest retail corridor. Again, no dent in Maggi’s share.

Attacking Maggi on its own turf, with the same product, same consumer, same price — doesn't work. No matter the distribution. No matter the budget.

2. Geographic and product attack.

One thing people didn’t like about Maggi was that it clumped together when cooled. Yippee went after this customer problem.

They launched in 2010 in Bengaluru, not Delhi. Reason? Maggi’s penetrations were the weakest in the south, and ITC’s network was strong here. Two variants entered the market. Classic masala, which the original Maggi lovers devoured and Magic Masala, which introduced a new taste to the Indian palate. People bought both.

When the 2015 ban wiped Maggi off shelves, ITC was ready. They doubled marketing spend, pushed retailer assurances directly, and positioned Yippee as the obvious alternative. When Maggi returned, Yippee had converted enough to hold. 20% share today, from zero in 2010.

Wai Wai applied the same logic to a harder geography — the Northeast, where even players like Maggi don’t have a stronghold.

CG Foods, the manufacturer of Wai Wai, solved this by manufacturing in the North East, making distribution logistics easier. But the sharper advantage was cultural — Wai Wai was already known in the Northeast before CG Foods formally entered India. Nepali students, border traders, and trekkers had been carrying it across for years. Demand was waiting. Northeast and East now account for 50-60% of Wai Wai’s total revenue in India.

3. Ideology attack

In 2015, Baba Ramdev had something no other Maggi challenger had. A following that looked almost identical to Maggi’s consumer base — rural, middle-class, price-sensitive households that had grown up trusting both his yoga and his product range.

Patanjali’s revenue had just crossed ₹5,000 crore, growing 150% in a single year. It was moving product through 4,700 exclusive outlets, including Big Bazaar and Reliance Retail — deep into the same kirana and modern trade network where Maggi lived.

Priced at ₹15 per pack, just below Maggi’s atta variant, and with an entire consumer base on standby, the economics made sense too. Plus, the timing was perfect: Maggi had just been banned, consumer trust was shattered, and the category was wide open.

But Patanjali couldn’t crack taste. A cumin, ginger, turmeric, herb-forward flavour — one consumer put it plainly: it “will always repel consumers from tasting it again.”

Then there was the regulatory problem. Patanjali launched the product without proper FSSAI approval, and a subsequent quality test found ash content in the tastemaker nearly three times the permissible limit. The brand that entered on a safety argument had its own.

The market that couldn’t be taken. Only surrounded.

The chips market is fragmented equally because no single player owns the occasion. Snacking is broad, low-loyalty & variety-seeking. Lays, Bingo, and Balaji carved pieces without displacing each other.

Noodles work differently.

Maggi created the category. The after-school snack, the late-night hunger fix, two minutes on a gas flame — these occasions didn’t exist before Maggi named them. By the time challengers arrived, the centre was occupied. Every brand that followed had to find a corner Maggi had left open.

That’s why the fragmentation looks the way it does. Yippee, found a product complaint and a geography. Wai Wai found a region. Patanjali found a crisis window and couldn’t hold it. No share was taken from Maggi directly. It was built in the gaps.

The brands still circling aren’t attacking Maggi either.

Ching’s colonised Desi Chinese at home — an occasion Maggi never owned. Korean ramen is riding a cultural wave at ₹100-150 a pack, speaking to a consumer Maggi has never spoken to. Yu Foodlabs is building a premium segment that didn’t exist five years ago. Different occasions, different consumers, different price points entirely.

Health noodles is the one space where the logic shifts.

Maggi has already tried it with Atta Noodles, Oats Noodles, and Nutri-licious. None moved meaningfully. Maggi’s brand memory is indulgence and comfort, and a health claim sitting on top of that memory doesn’t fully land.

WickedGud and Slurrp Farm don’t carry that baggage because their entire identity is the health positioning. The catch: the moment health noodles becomes large enough to matter, Maggi has the distribution and consumer trust to flood the segment, possibly under a separate brand. That race is still open.

very well written

Maggi will always own the crown. Yippee is good, but not that top of the mind. Slurrp Farm has ruined its Hakka noodles by adding rosemary (besides being too high-priced for daily consumption), and its instant noodles leave my mouth dry, unlike Maggi, especially its atta noodles. Wai-Wai is an acquired taste; Maggi has no such threshold to cross. There's also the matter of conditioning because I want the same taste attached to pleasant childhood memories. These are hurdles that are hard to overcome, and it may take more than a generation to topple the queen/king.