Haldiram's 10% stake sale, Zepto's base shift to India & Atomberg's ₹1000 Cr. Fan Playbook 💡

Insights from India’s top consumption-driven companies.

We are back after a long 2-week break. Today’s edition covers three important business topics: Haldiram’s 10% stake sale at a ₹80,000 Cr. valuation, why Zepto is shifting its holding entity to India, and insights behind Atomberg’s ₹1000 Cr. fan empire.

Haldiram-Temasek $10 Billion Deal💰

First, some context.

The desi 80+-year-old snack giant has created an empire that makes more than ₹14,000 Cr. in combined group revenue. There have been reports of a term sheet coming into place between Haldriams & Temasek (the mighty Singapore-based sovereign wealth fund) for 10% at ₹80,000 Cr. valuation.Not the first time.

This isn’t new—over the last decade, the family has been approached by top PE firms and FMCG giants like Tata, Pepsi, Bain Capital, Warburg Pincus, Blackstone, and others. It’ll be interesting to see if things finally materialise, as there’s significant ROI potential in the OFS (offer-for-sale) for the upcoming IPO, which is on the cards for quite sometime.

Fact: Any non-promoter investor with a 10% stake can be part of OFS as per BSE guidelines. So 10% stake puts PE players in the right spot to offload some in IPO..

Why is it a big?

Well, because it is probably one of the most valued private companies in the country. For context, 2X the valuation of Zepto. They have a 35% market share in the ethnic snack segment and ~13% share in the overall snack segment, making them bigger than the combined market share of the next 5 players (Balaji, Bikaji, Bikanerwala, and others).

What can we see?

The snack business drives 85% of revenue, with QSR contributing 15%, but the QSR segment shows strong growth potential. There’s significant scope for expansion in Tier 1 and Tier 2 cities as the food sector becomes more organized. International markets also hold promise, driven by strong trust and brand recall. Plus, the company has introduced premium categories like chocolates and upgraded to more fancy stores, to add a touch of premiumisation.

Zepto’s homecoming pre-IPO 🇮🇳

First, some context.

Zepto is shifting its main parent entity to India before the IPO. How? By a reverse merger with the current holding parent company (in Singapore). For this, it has set up a new entity, Zepto Marketplace Pvt. Ltd., as the main ultimate parent. The restructuring has received approval from Singapore and is yet to go through the National Company Law Tribunal later in the month.

But, why all this effort?

Zepto wants to avoid all sorts of government intrusion by moving to a marketplace model with this entity. Why? Well, because the Government allows 100% FDI in the case of a marketplace-led model and prohibits it completely under an inventory-led model where you can hold your entity.So far, Zepto has used a B2B2C model — where Zepto’s parent entity (Kiranakart) works as a B2B entity – it buys goods from brands to later sell it to a few license companies. This licensee later sells goods on the platform to customers. The licensees pay a fee for using Zepto’s brand and platform and Zepto takes care of procurement and branding. Btw, Zomato and Swiggy are already using a marketplace model with a different touch of nuance, which we can discuss some other day.

The domicile shift wave.

This is a common trend. Many startups—like Razorpay, Flipkart, Groww, and PhonePe—set up baseS in Singapore or other countries. They transfer ownership to a foreign entity & have a wholly-owned subsidiary in India. The logic for Singapore is clear: Singapore offers zero capital gains tax, no dividend tax, and one of the world’s lowest corporate tax rates (17% vs. India’s 25%+). Access to capital and VC preferences also play a key role. That said, reverse flipping now makes sense, especially with strong tailwinds in public markets.

Fact: Currently ~8000 Indian companies are registered in Singapore.

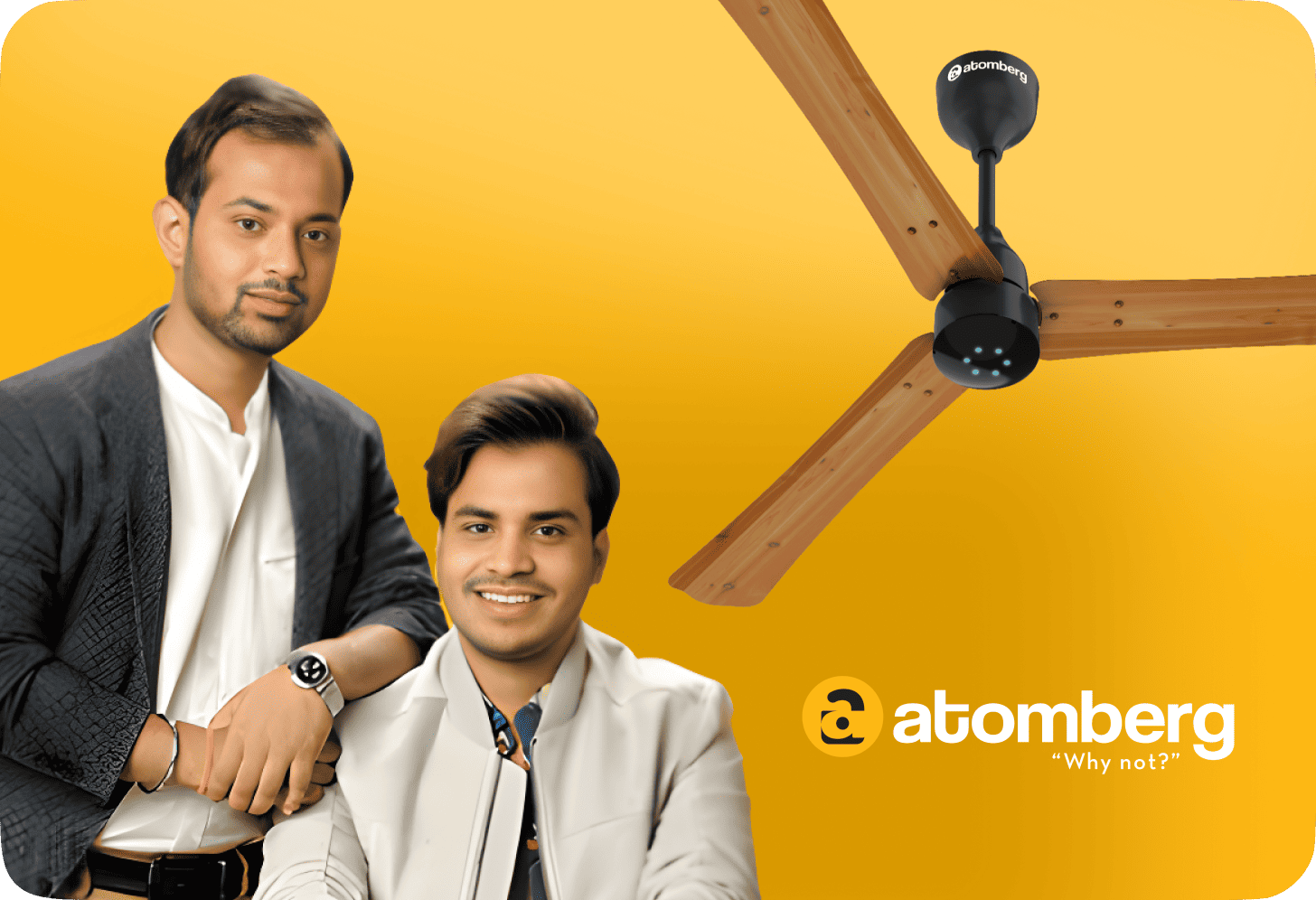

Atomberg’s ₹1000 Cr. Fan Playbook 💡

First, some context.

Atomberg is a D2C startup that makes more ₹1000 Crores in yearly revenue in a crowded unsexy space and has become the “Tesla” of fans in India. The interesting part? they created a category in a space dominated by legacy giants like Usha, Bajaj, Orient, Crompton, Havells.

What did they crack?

Finding a whitespace.

Atomberg brought BLDC (Brushless Direct Current) motors while everyone was using induction motors. BLDC produced less heat, allowed more sleek designs, and led to long-term cost savings by consuming less electricity. For ex— 35W compared to 70 to 80W. But why did no one bring this before? Simple: margins. Importing magnets & electric printed circuit boards from China for these motors would lower margins. Plus, there wasn’t enough customer education to justify paying a premium for this.Premiumisation.

Over this, Atomberg added a layer of all smart features like fancy modern futuristic shapes, google & remote control. Remote control became a big hook for customers. The idea is simple: Add more premium features → Hook customers with something no one else in the market offers → Show them the practical rationale → make them pay for premium.B2B before B2C.

Before going all in on e-commerce and offline channels, Atomberg used a “Veeba-like” approach of going B2B first. They targeted ceramic industries playing on cost angle and later also got corporate clients like Tata Group, Infosys, and Indian Railways.What’s ahead?

The company is executing a narrow-to-wide strategy, adding categories like mixers and smart locks. This is crucial as they target the growth from ₹1,000 Cr to ₹10,000 Cr. What’s crucial is launching products that meet the highest tech expectations of their ICPs.

By the way, sometime back, we hosted Arindam Paul, the CBO of Atomberg, for our weekly deep dives. He shared great insights on how to crack marketplaces as a DTC brand today.

That’s all for now. Last month, we had a stellar line-up of leaders who taught GrowthX members specific nuances across product building, distribution, and strategy.

Mihir Bhanushali (Regional Sales Head, Whatfix)

Gautham Krishnan (Product leader, Disney+ Hotstar)

Ajay (Global Field Marketing & Events, Everstage)

Deepika (Senior Manager, Field Marketing at Whatfix)

Nivas (Head of Marketing, Spendflo. Ex-Freshworks)

Pramod N (VP Head of Product & Data Science)

If you work in a product or marketing role, come join us and make learning a core habit every week in this fast-moving tech world.

Thanks for reading GrowthX's Newsletter! Subscribe for free to receive new posts and support our work.