Can WhatsApp Pay break the UPI duopoly?

And where WhatsApp can play to win.

Before we begin...here’s a career cheat code.

Want to accelerate your career? Become an AI-native worker. Use AI to automate busywork, think better, communicate clearly, and ship more.

The people doing it are already inside GrowthX, building real projects every week.

Build sprints. Expert-led sessions. AI credits. Feedback. A community that pushes you to ship. GrowthX has everything you need. What’s your excuse?

Today’s edition

‘Superior sales and distribution can create a monopoly, even with no product differentiation.’ Peter Thiel wrote that in Zero to One. Anyone tracking WhatsApp Pay knows that the opinion isn’t holding.

For context, WhatsApp has over 500 million users in India. By Thiel’s logic, WhatsApp should have buried PhonePe and Google Pay years ago. Instead, WhatsApp Pay’s UPI share sits at 0.65% today — a number it’s trying to grow desperately. Why is that?

The truth behind WhatsApp Pay’s market share numbers.

WhatsApp Pay entered India’s UPI market in early 2018. By then, PhonePe had already been live for 18 months. Google Pay, then still called Tez, for six.

NPCI (National Payments Corporation of India, the organisation pioneering India’s cashless movement) capped WhatsApp at one million users the same day it launched. But why? It wasn’t a standard policy then. Plus, PhonePe and Google Pay avoided it entirely.

So why the cap on WhatsApp specifically?

All UPI-based apps — PhonePe, GPay, Paytm, and WhatsApp — plug into NPCI’s shared TPAP system to process transactions. A brand-new entrant on shared infrastructure carries real risk: one rogue line of code could jam the rails every other app depends on too. Besides, WhatsApp had a bigger market than PhonePe and Google Pay combined. It could simply roll out the product to all its users, crashing systems quicker.

So, WhatsApp’s pilot, run with ICICI Bank, got treated as a new, unproven system, sandboxed at a small, contained scale before anyone trusted it with more.

The data rules behind WhatsApp’s 5-year slow start.

RBI’s rule was simple on paper: payment data stays in India.

Think about it.

If a transaction fails, or fraud shows up, or a court needs records, RBI wants to walk in and pull that data itself, no waiting on a foreign company’s legal process, no depending on another country’s courts to grant access. Data sitting abroad means jurisdiction sitting abroad too.

WhatsApp’s competition were unscathed by the rules.

PhonePe and Google Pay were built in India, on India-based infrastructure, from day one. Clearing that rule cost them nothing.

Meanwhile, WhatsApp’s payments system ran on Facebook’s global cloud.

That’s the same infrastructure carrying chats and contacts for hundreds of millions of users worldwide. Separating one product’s data from that system would take years. For WhatsApp, it took two, before NPCI relented.

The cashless explosion.

Transaction value more than doubled in a single year during the same time the pandemic struck. Two apps, PhonePe and Google Pay, were suddenly moving 80% of cashless transactions.

NPCI looked at that number and decided it needed real rules, fast. So, in November 2020, it introduced a 30% cap for incumbents and a formal, phased rollout for new entrants.

After years of being capped at 1M users, WhatsApp Pay couldn’t roll out to everyone.

First, the rollout would be to twenty million users. Then forty. Then a hundred, by 2022. Fully open only in January 2025. By that time, PhonePe already owned 47.8% of the market, and GPay owned 37%.

Is there a way WhatsApp can capture market share now?

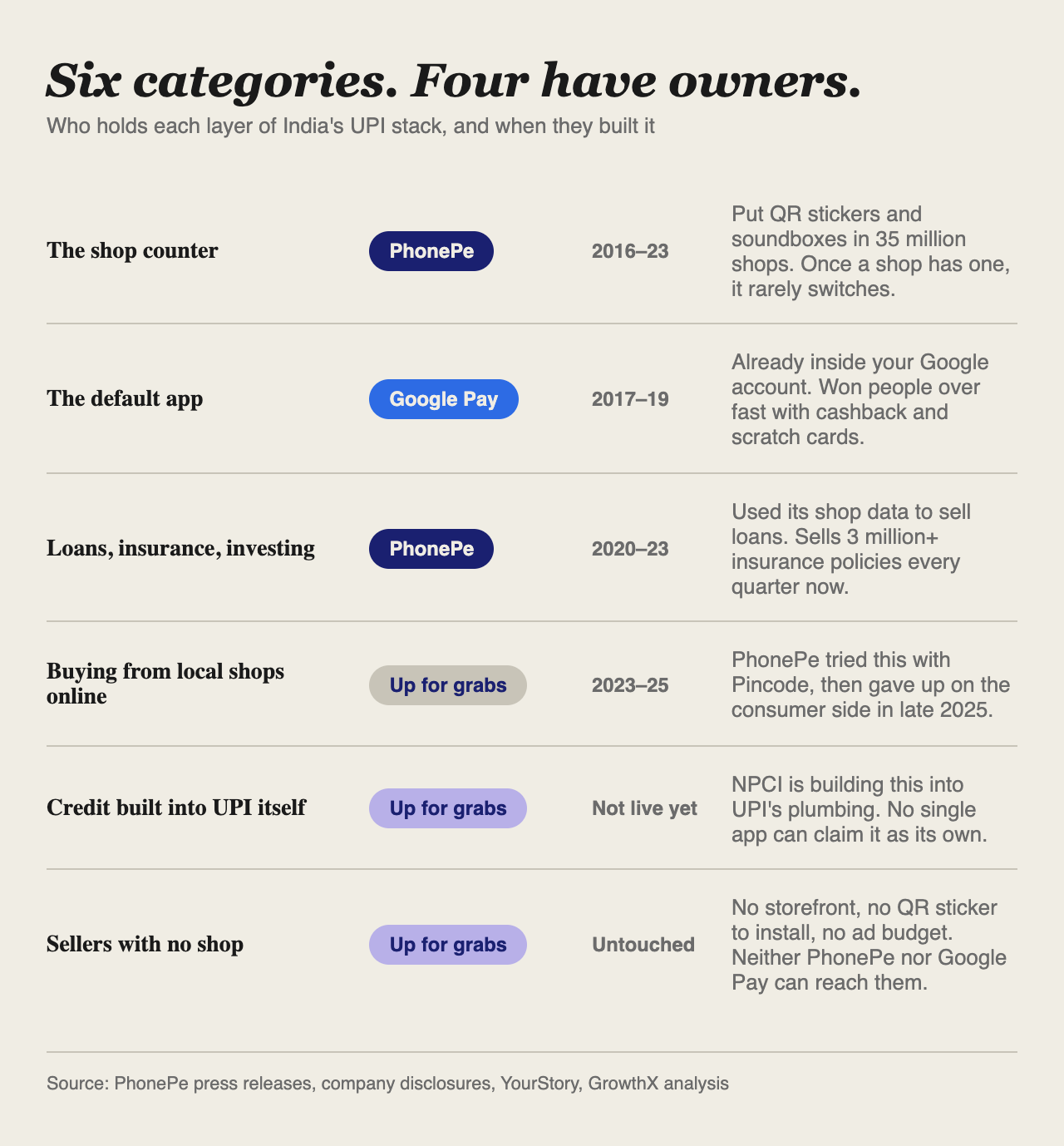

Let’s look at the UPI payment categories being disrupted.

Where does WhatsApp really fit in?

Here are the categories WhatsApp can disrupt.

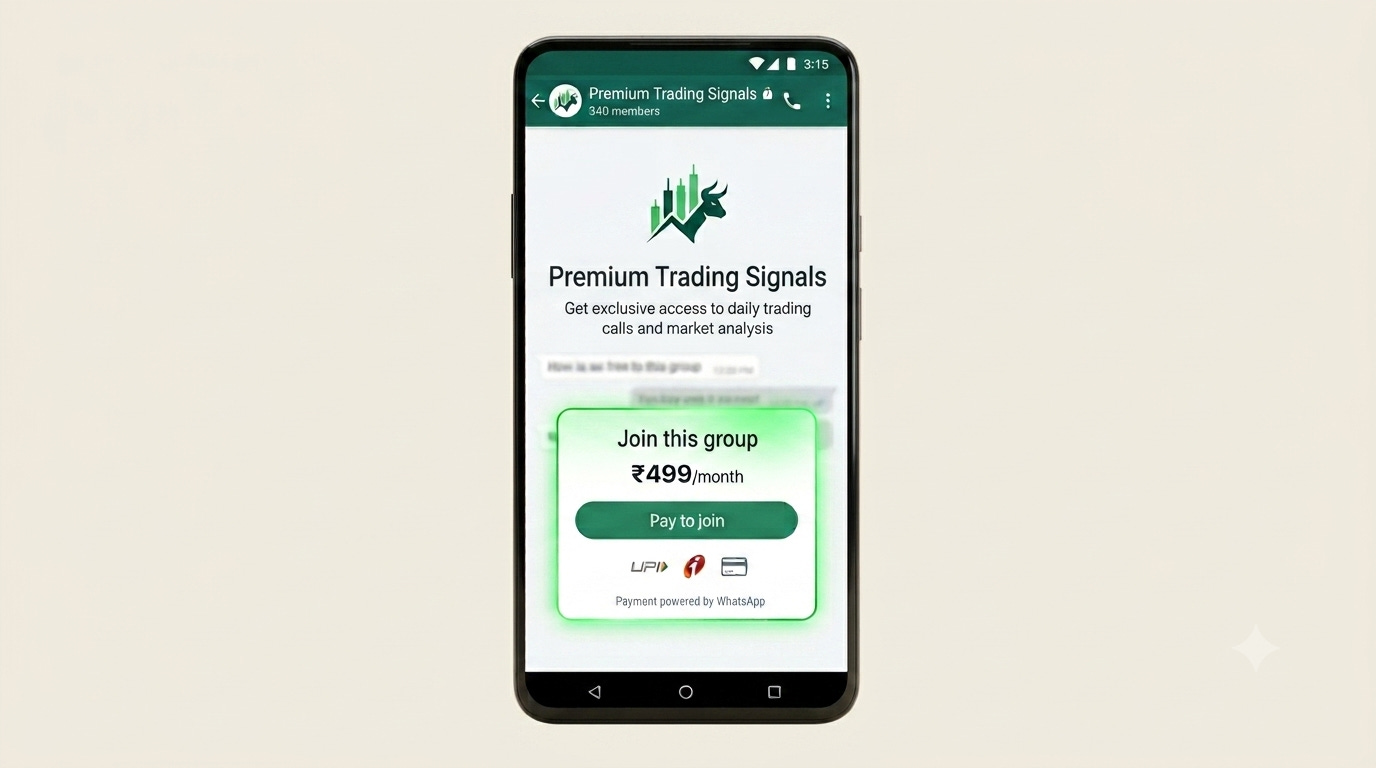

1. Paid community subscriptions

There’s a small industry that exists for one reason: helping people charge for access to a WhatsApp group. Tools like CommuniPass handle the paywall, run the billing, remove members who stop paying. WhatsApp itself never built a native way to do any of this.

Now it’s about to. Meta is rolling out paid subscriptions for Channels through 2026, taking a flat 10% cut.

Here’s the problem with that pitch. The workaround isn’t free; it runs on a monthly subscription plus a small percentage fee, but it’s still cheaper than Meta’s cut.

So, the million-dollar question then is: why would anyone switch to WhatsApp?

a. Friction.

Every third-party tool still has to send the payer out of WhatsApp to a Stripe checkout page before bringing them back in. If that experience is tedious, there’s a good chance you lose out on a paying customer forever.

A native subscription closes that gap entirely: no redirect, no separate tab. The whole loop is seamless, all within the channel where the interaction first started.

b. Discovery.

CommuniPass has no browse page, no directory, nothing for a stranger to stumble onto. Every subscriber has to be imported from somewhere else. WhatsApp’s Channels already ships with a built-in directory, browsable by what’s new, most active, most popular, filtered automatically by country. A creator with zero external following can still get found just by sitting inside WhatsApp’s own discovery surface.

c. Brute force.

This is the unfair one of the lot. Meta has already shown it’s willing to use policy, not product quality, to clear a lane once it decides to compete in it. In January 2026, it banned general-purpose AI chatbots from WhatsApp’s own Business API, right as it pushed Meta AI as the platform’s native assistant, while leaving ordinary business-use AI untouched. Will WhatsApp actually take this route? Time will tell.

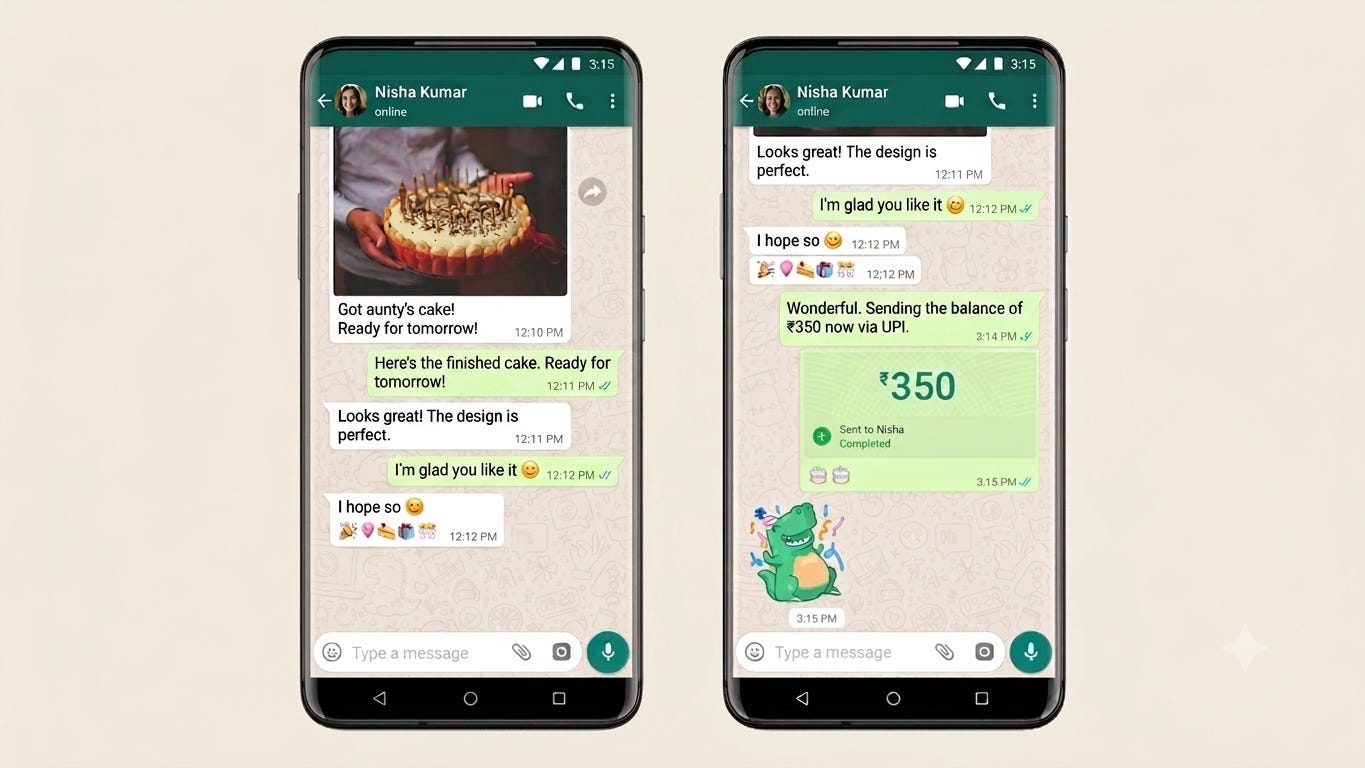

2. Merchant payments.

PhonePe and Paytm have both done this before, at real scale, with physical hardware pushed shop to shop. Paytm alone has built a 37 million-strong merchant network, QR codes and soundboxes, and field executives going door-to-door to get devices installed. The catch? A Paytm device needs a counter to sit on. And many sellers still operate informally on WhatsApp.

This is who WhatsApp could serve. Most of the ecosystem is already there. The catalogue exists, up to 500 products, browsable inside chat. The negotiation layer exists, the actual back-and-forth, “is this in stock,” “can you do a discount,” happening in the same thread the sale closes in. The only thing missing is WhatsApp closing the loop rather than a third party.

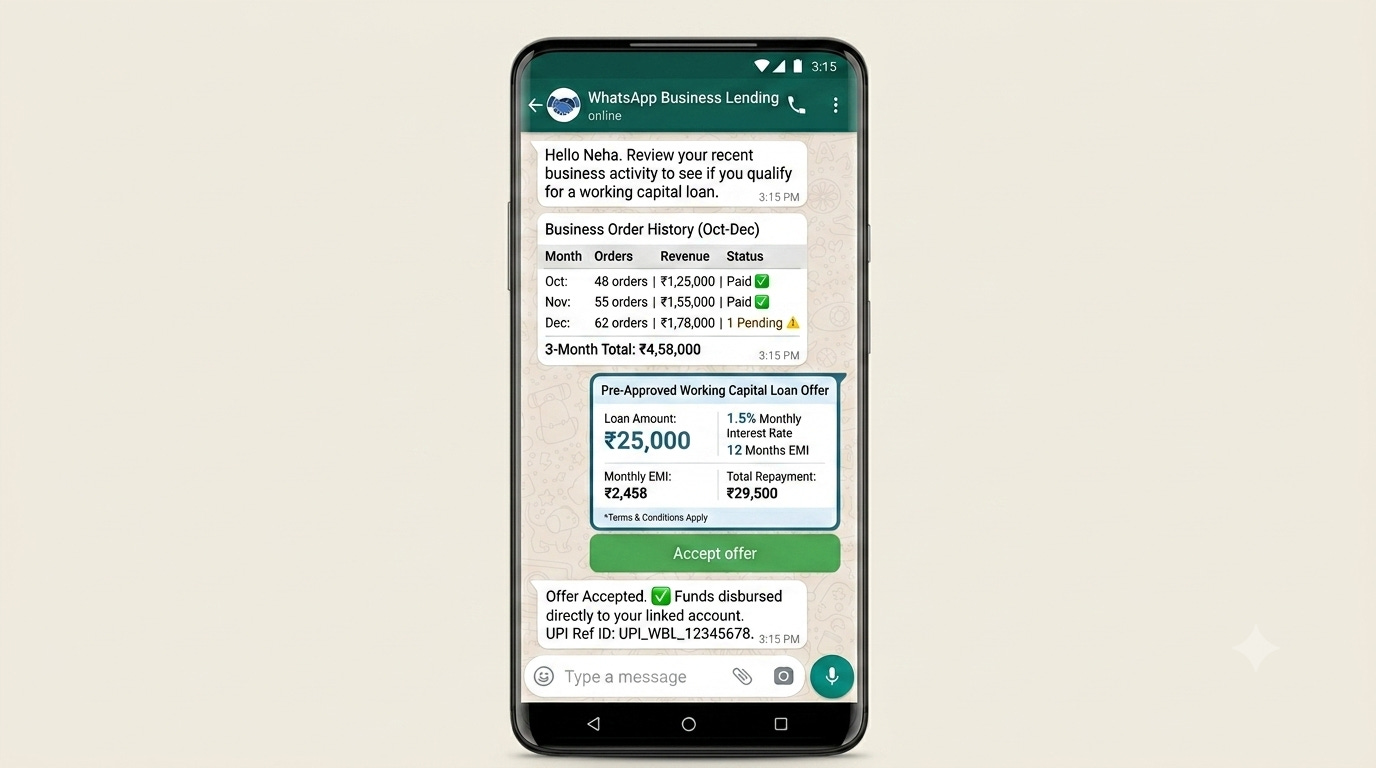

3. Merchant lending.

Most MSMEs shut out of formal credit don’t simply go without it; they end up with unregulated lenders charging 24 to 36% annual interest because nobody with better terms can actually underwrite them. WhatsApp could cater to this audience too.

The tool already runs the plumbing to pull it off. Every order placed through its native commerce flow generates itemised totals, payment status, a reference ID, structured data sitting right inside the message objects themselves, arguably richer than a PhonePe soundbox log, which only ever captures a payment amount. That’s the exact data a lender would underwrite against, every single day, for every merchant running a catalogue through it.

What it hasn’t done yet is decide what to do with that data once a transaction closes. Right now it passes through and disappears, treated as disposable.

Besides, WhatsApp would still need a regulatory shell to run lending on its platform. A payment aggregator license, the kind the RBI cleared for CRED in March 2026? That’s something WhatsApp could use to process merchant payments at lending scale.

On June 22, Meta appointed Kunal Shah as WhatsApp’s CEO. Meaning, expanding WhatsApp Pay’s 0.65% market share now falls on his shoulders.

Kunal has successfully acquired users for CRED. But it was a different company, catering to the top 10% of India. Kunal must think for the 90% now. Whether he can do that successfully is an open question.

Want to plug your brand into our newsletter?

Email us at collab@growthx.club

I keep thinking about the informal merchant angle here. The payment redirect to a third-party UPI app is genuinely the only clunky step in that experience. If WhatsApp Pay can close that loop natively, the 0.65% figure starts to look like a starting line rather than a ceiling. The real race isn't against PhonePe, it's against the merchant habits PhonePe's business tools are building with those same sellers right now.

Great breakdown

(I really didn't understand this MSMEs lending problem though)