Breaking insurance rules made ACKO ₹2,837 Cr.

It's changing how ~200 Mn Indians buy insurance.

What do you call it when you build something, don’t know how it works, and you’re too afraid to make an update? Answer: Regular vibe coding.

At GrowthX, we put you in rooms with people who went from prompt to paying customers so that you can exchange notes and get to iteration #1 faster. Want in?

Today’s edition.

Up until recently, your parents and grandparents bought insurance the exact same way, either through an agent or a family friend who knew what they were doing. For over 70 years, every player who entered defaulted to the exact same model.

Then, in 2016, ACKO challenged conventions by building its entire company around selling insurance without agents. In 2025, they made ~₹2,837 Cr. in revenue. How on earth did that happen?

Why every insurer still pays the middleman tax.

Here’s what the insurance product really is: It’s a dense document that asks you to pay money up front for an emergency that may (or may not) strike.

It’s not a product that sells itself, especially to a population where financial literacy is still ~27% in 2025. This is exactly why LIC needed agents to meet prospects, discuss policy documents over chai to make a real sale in 1956.

Post 2000, private insurers flooded in, and the market got commoditised. ICICI Lombard, HDFC Ergo, and Tata AIG all sold the same product. Agents now serve a slightly different purpose. Since insurance is a push product, they still had to go to customers to sell it. But now they’d also show them why one product was better than the other.

Result? Legacy insurers and incumbents pay higher commissions to middlemen to ensure their products get distributed.

ACKO’s thesis: Own distribution, fire the agent.

Before Varun Dua founded ACKO in 2016, he was at Coverfox, an insurance marketplace like PolicyBazaar. He learned one thing over his stint:

In insurance, people are hostages to agents. These middlemen hold power over customer decisions, such as buying and renewals, as well as customer data. Without agents, the insurer has nothing.

This insight gave rise to ACKO.

5 ways ACKO wanted to change how insurance worked in India.

1. Own the customer

Skip the intermediaries and access the customer directly. With that, two things happen. The insurer gets more control over a customer's decision-making. Unlike a broker/agent, they can directly show their policy range to customers. And two, they can offer better personalised pricing to every customer — something no agent does right now.

Wait, what’s wrong with current pricing?

Agents sell an insurers insurance in cohorts. Each customer in the cohort gets the product for the same price. The idea here is simple. The risk averages out.

Meaning, if one cohort has individuals who never take on risks and never file claims as well as people who file a claim, everyone still pays the same premium. This pooled premium gets used when someone files a claim. Long story short, there’s no real benefit for a financially healthy, low claim-filer to get this insurance.

2. Fixing insurance economics.

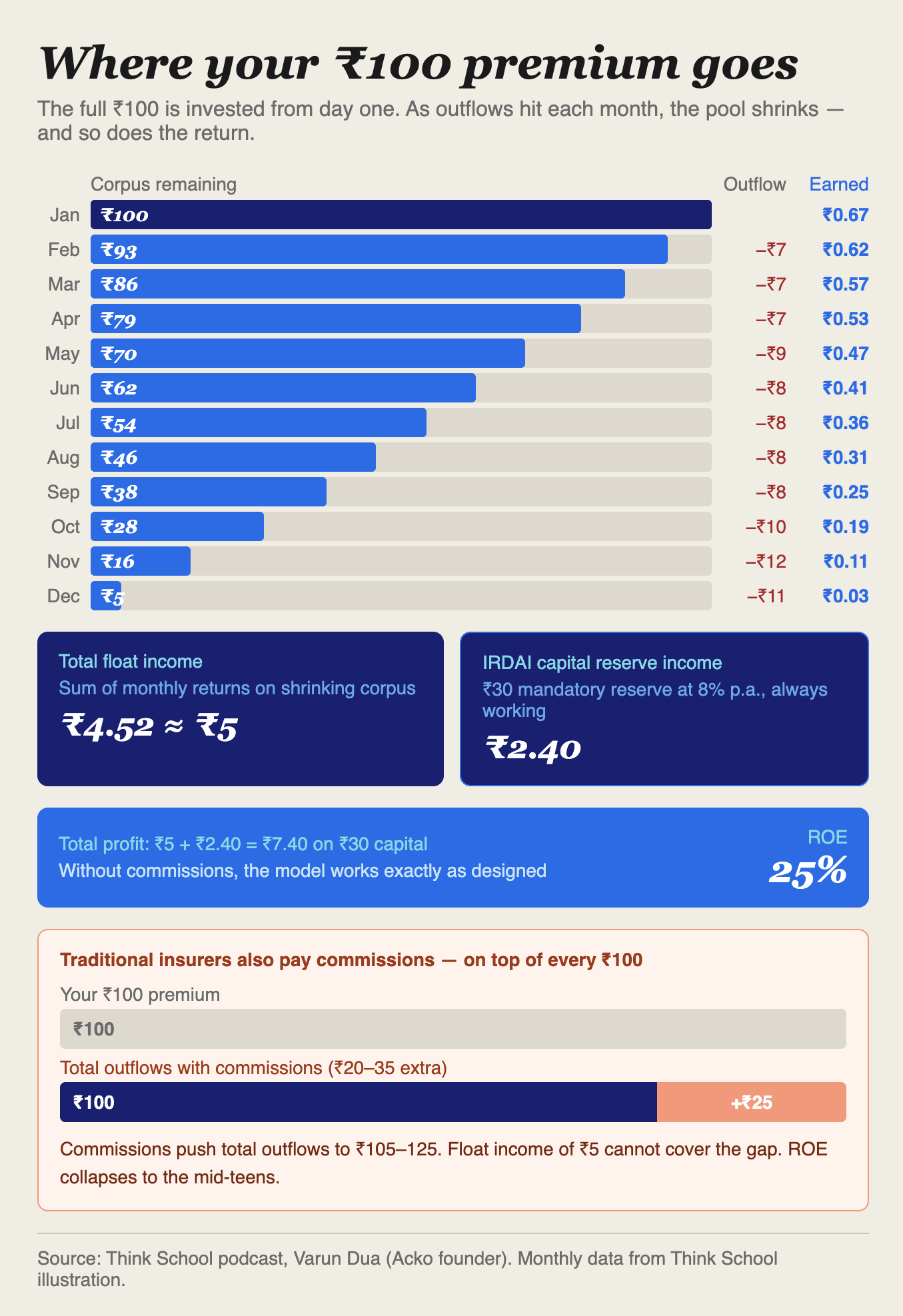

The chart above shows the best-case scenario. The full ₹100 invested from day one, outflows draining slowly, each month’s balance earning its share of the 8% annual yield. Total float income: ₹4.52. Add the reserve income, and you get ₹7.40 on ₹30 deployed — a 25% ROE (Return on Equity).

That math holds only when claims don’t arrive. The moment a large claim hits, the corpus drains faster than the model assumes. Add commissions on top, and total outflows regularly hit ₹105-108. The float income of ₹5 disappears into the underwriting loss before it reaches the bottom line.

Varun at ACKO is building a model to reach a claims-free book. The key differentiator? Pricing individually.

When ACKO prices each customer individually using route data, driving frequency, and claims history, it isn’t just charging the right premium. It’s selecting for the customers least likely to claim. Build enough of those into your portfolio, and the corpus drains slowly, the float stays large, and the 25% ROE stops being theoretical.

Firing the agent removes the commission. Individual pricing builds the right book. Together, they make the insurance gold mine work.

3. Rebuild the product.

India spent 40 years buying insurance as a savings vehicle. LIC sold endowment plans. Private insurers sold ULIPs. The product was always: pay in, get money back.

Varun wanted to change what insurance means to the consumer. His vision? Make insurance what it always was: a protection tool for a family that has assets to protect and risks to cover.

The target was the 100-200 million digitally savvy Indians already thinking about financial products differently. For them, the agent’s pitch of “you’ll get ₹13 lakhs back in ten years” was already starting to feel like a bad deal compared to a mutual fund. They were ready for pure protection if someone offered it honestly.

4. Embed the customer deeply into your ecosystem.

Think about it from ACKO’s POV. A person who buys car insurance from ACKO at 28 will also need health cover when their parents age, and term life when they have children. Every insurance purchase from ACKO then adds a layer of data — claims behaviour, health history, renewal patterns. So, the next product is cheaper to underwrite and easier to price. Plus, the acquisition cost goes down since you’re compounding on the person’s past purchases and experiences with you.

The logic is sound, and all the math works when you figure out how to really replace the middleman.

The middleman replacement.

One American insurer, GEICO, has sold insurance without agents since the 1940s and managed to remain profitable. They first sold via direct mail, then by phone, and then through the internet.

The model was always the same: remove the middleman, pass the savings to the customer, and spend heavily on advertising to replace the awareness the agent used to create. By 2024, GEICO’s expense ratio was 9.7% — the lowest of any major insurer in the US.

Varun saw an opportunity to replicate the same playbook for India.

Behind ACKO’s agent-less playbook

Why motor first?

When you remove the agent, you lose the one person who vouched for you. The first product you sell has to require the least trust to close — and carry the lowest risk for the customer trying you for the first time.

Every car on the road is legally required to carry insurance. Plus, the premiums are low — typically ₹3,000-15,000 annually — making it the smallest financial bet a customer makes on a new brand. Unlike health insurance, where medical history and waiting periods lock customers in, motor customers move freely on price and service. So, even if ACKO gets it wrong, the customer simply leaves next year. Nothing catastrophic happens.

This is a classic beachhead strategy. Find the segment where your biggest disadvantage (in this case, no agent network) matters least. Establish there. Build data, build claims track record, build renewals. Then move up.

One problem. Even motor insurance renews only once a year. Meaning that no matter the launch time, it would take at least a year to get people to even consider ACKO as a replacement insurance product.

Solving the recall problem with micro-insurance.

The Ola trip cover in April. The Amazon device protection in August. Each one puts ACKO in front of a customer at a moment when they weren’t thinking about insurance and weren’t being asked to make a significant financial decision. A ₹1 tap on an Ola checkout requires no trust, no comparison, no conviction. It just requires not saying no.

But the effect compounds. By the time the motor renewal arrives in January, ACKO isn’t a cold name on a comparison website. It’s the company that covered the Ola ride, the company that protected the phone.

Wait, does the ₹1 insurance make business sense for ACKO?

Yes, the math works out thanks to partnerships.

If there’s a 1% chance a phone screen breaks and repair costs ₹3,000, the risk price is ₹30. Meaning, you’d had to collect ₹30 from every 100 people to make the math work. ACKO collects only ₹1 though.

The rest ₹2,900 most likely comes from platform sfees, float revenue, and underwiting revenue from not paying middlemen commissions to distribute their products. So far, ACKO has earned profits qorth ₹800 Cr.+ by enabling people to buy more micro-insurance.

Why health next?

The market case was obvious. Health insurance GWP was growing at 15-18% annually — nearly double motor’s 10-13%. Plus, when customers bought health insurance, they rarely switched due to the tedious waiting periods. That made health the ideal next market to conquer.

The problem? Unlike motor, health has no low-trust entry point. People don’t automatically trust a motor insurer to also offer reliable health insurance coverage. Besides, they expect a new insurer not to have a hospital network, cashless tie-ups, or a 24/7 claims infrastructure, removing them from the consideration stage entirely.

So, ACKO’s answer was to not sell retail health at all — at first. In 2020, it entered the corporate group health market, selling policies to employers. Within two years, Swiggy, Razorpay, and CRED were on the books. The hospital network got built. And claims infrastructure got tested at scale. The brand earned its health credibility before retail customers were asked to bet their family on it.

Retail health launched in 2023. By then, 50% of those customers were already Acko motor policyholders. The acquisition cost on that conversion was close to zero.

But now, everyone who bought the health insurance actually needed it, which was terrible for profitability.

Why insurers are wary of distributing health insurance.

At the time of purchase, the insurer knows quite a lot. They have a detailed questionnaire, declared pre-existing conditions, family history, and lifestyle factors from before purchasing the insurance.

They can’t see whether a customer who was healthy at 32 when they bought the policy became progressively more sedentary over three years. Or whether their blood pressure, blood sugar, or both started rising.

This is exactly why ACKO acquired OneCare, a chronic care management company. The idea was straightforward. Allow customers to receive continuous health monitoring instead of a one-time checkup, and provide predictive data whenever a health condition worsens. Early diagnosis > Lesser hospital spending > Lower claims amount.

Is ACKO’s business model good for India?

From a peak loss of ₹738 crore in FY23, ACKO has cut its net loss to ₹424 crore in FY25 — a 43% reduction while revenue grew 35% to ₹2,837 crore. Expenses grew only 17% in the same period. The operating leverage is showing. Motor is at break-even. Advertising spend, ACKO’s largest acquisition cost, fell 12% even as the customer base grew.

But there’s still a cloud that surrounds ACKO.

GEICO’s model worked because it entered a market where demand already existed. GEICO didn’t manufacture that belief — it just made buying cheaper and easier. Compare that with India for a second. Non-life insurance penetration sits at 1% of GDP, unchanged in a decade despite every insurer and every agent pushing in the same direction. The demand infrastructure that made GEICO possible doesn’t exist here yet.

ACKO has appointed Morgan Stanley, ICICI Securities, and Kotak Mahindra Capital for an IPO targeting $2-2.5 billion, with a listing expected in early 2027. The public market will price all of this simultaneously — the improving trajectory, the structural constraint, and the bet that Indian insurance literacy is catching up. ACKO has until 2027 to make the same case.

Great breakdown