Blinkit's robbing FirstCry of ₹1380 Cr.

And it's coming for beauty, pet care and pharmacies next.

8 hours. 120 builders. ₹3.5 lacs in cash up for grabs. One condition: build a Voice AI app that moves your bottom line, not just your demo.

Credits, fuel, focus rooms, and mentors — everything is covered. Up for the challenge?

Today’s edition.

FirstCry generated ₹8,547 Cr in consolidated revenue last year. Strollers, school bags, formula, and birthday party supplies. FirstCry takes care of everything until age ~10. 11 million customers transacted on the platform.

Diapers are 15% of everything that was bought. ₹1,380 Cr annually.

Blinkit and Zepto have started eating into that number. Now, the management’s worried, too. Why is that?

The real mechanics of a baby retail store.

Get customers into the ecosystem with low-margin, high-frequency products. Make them stay to buy the high-margin considered purchases. For a baby retail store like FirstCry, diapers are the product that gets customers into the ecosystem. Which is why FirstCry typically doesn’t shy away from greater discounting — all to own that customer visit.

Margins? FirstCry earns 15-20% on diapers compared to 25 - 50% on everything else.

That’s where the similarity between baby retail stores and regular retail stores ends. Baby retail has a problem that no retail stores do — their customer cycles quicker.

The tale of the cycling customer.

Here’s the thing about babies — they grow up.

Meaning a baby retail store becomes obsolete 100% of its target customer base in just a few years. The store must do two things: maintain a steady supply of new customers and consistently be their no.1 place to shop for baby products.

Once the customer enters the ecosystem, and more importantly, likes it, the economics look great.

Think about it. For two and a half years, the parents have returned every fortnight like clockwork. No marketing spend. The diaper runs out, and they’re back.

The problem? Habit doesn’t earn margins.

Then the diapers stop too.

The parent who visited weekly now comes in once every few months for a birthday or a season change. What was a self-sustaining retention loop now requires active effort in the form of promotions, reminders, and reasons to return that the product no longer provides on its own. The retailer has to earn every visit it used to get for free.

Most baby retailers die before they figure all of that out.

The baby retail graveyard.

Before FirstCry came in, the market was brutal.

Organised baby retail wasn’t store-based. Most parents bought from local kiranas, chemists, and grey importers who had no real cost structure and no need to justify margins.

This meant:

1. CAC was higher: Customers don’t know you exist, AND don’t trust you.

2. Working capital requirements were through the roof: Stores need a replicable experience — with inventory buffers, return policies, and multiple payment modes while competing on price.

Hushbabies launched in 2009, the earliest of the lot. Entirely online, entirely dependent on its next funding round, and with no mechanism that made it structurally harder to replace than any other e-commerce tab.

BabyOye launched in 2010 and had better fundamentals — 13,000 products, $14.5M raised, and a recognisable brand. But it was metro-first and online-only at a time when half of India’s new parents lived in towns no delivery network reliably reached.

Mahindra’s Mom & Me, also launched in 2009, had the opposite problem. It had stores — 115 of them across 45+ cities. But 104 were company-owned. Every new location was a capital commitment on Mahindra’s balance sheet, which meant expansion was slow, expensive, and concentrated in cities where real estate justified the spend.

A retailer could only be profitable if it solved for customer acquisition, frequency, LTV, all while taking care of store economics. That’s exactly what FirstCry did.

1. FirstCry went where the customers were.

They went to hospitals, the one place parents were before they even thought about baby care. AT hospitals.

The gift hamper programme reached 16.8 million parents across 13,000+ hospitals in 514 cities. A curated box of samples and coupons, handed to a new mother before she’d opened a browser, sealed the acquisition.

2. Diapers solved for frequency.

The category became the reason parents visited FirstCry right after birth. They stocked the right range and offered them great prices, even at the cost of margins.

3. The platform fixed the LTV.

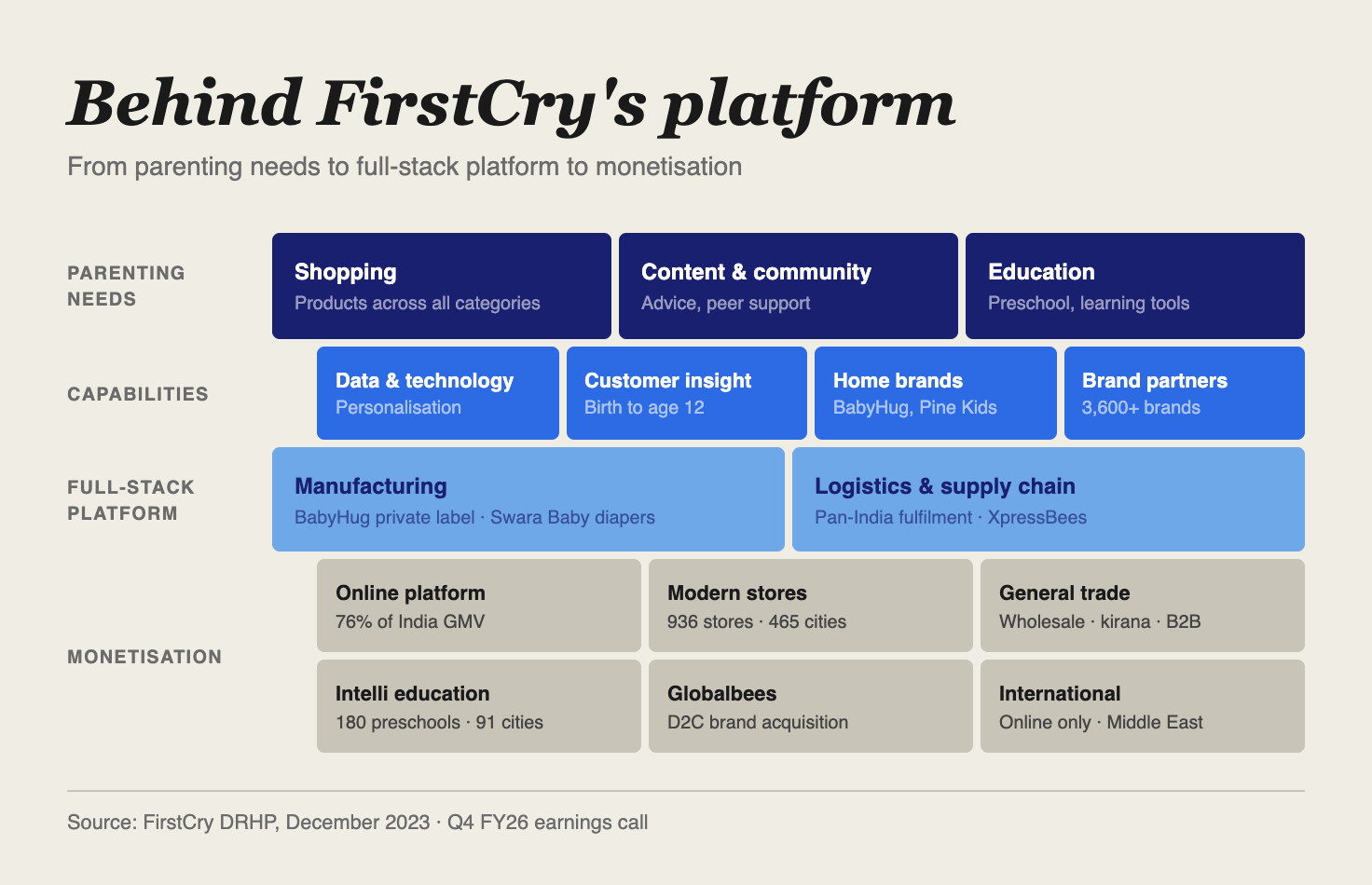

If you look closely at the image above, you’d notice that FirstCry goes beyond being simply a baby retailer. It offers support throughout the parenting journey through content, community and learning tools.

More visits = more upsells = more revenue.

4. Tier 2, tier 3 franchising solved shop economics.

FirstCry went offline in 2011 — but deliberately started in Tier-2 and Tier-3 cities, not metros, and built almost entirely on a FOFO (franchise-owned, franchise-operated) model. FirstCry provides the brand, inventory access, supply chain, technology, and marketing support. FirstCry collects a ~5-6% royalty on sales without carrying any of the store’s capital risk.

FirstCry’s revenues were already coming from small towns by 2013 — the same towns BabyOye couldn’t reach and Mahindra couldn’t afford to enter.

Now, q-comm is eating FirstCry’s frequency lever.

It’s happening on two levels — growth and margins.

First, quick commerce is making it easier for new parents to buy diapers. They typically have all the big brands, offer discounted prices, and, along with the other grocery items, typically free delivery, which is also available in 10 minutes.

FirstCry has tried to recover some traction by offering quick deliveries. QUIC launched in 5 cities, capturing 20% of online orders in active catchments. RocketBees expanded to 62 cities, accounting for 40%+ of online volumes. But the problem lies somewhere else entirely.

FirstCry has a ceiling for discounting. After all, it must make a margin. Stores like Blinkit or Zepto don’t have those concerns. They’re earning margins from entirely different places.

Plus, when Blinkit takes the diaper run, it doesn’t take one transaction. It takes the session. The app that’s already open when the parent needs the next thing is the app that wins the considered purchase.

FirstCry isn’t the first, and it certainly isn’t the last.

See, q-commerce is built on grocery frequency. The average urban household opens Blinkit or Zepto three to four times a week to buy milk, vegetables, and snacks. The app is already open. The dark store already has the inventory. The delivery fee is already being absorbed. At that point, adding diapers, pet food, or a face wash to the cart costs the consumer almost nothing.

That’s what vertical retailers are actually competing against.

Nykaa doesn’t lose because Blinkit has better beauty products. It loses because a parent who’s already ordering groceries doesn’t need a separate reason to restock her shampoo. The purchase in question, like a luxury fragrance, still requires discovery, curation, and the kind of intent that sends someone specifically to Nykaa.

But the replenishment purchase, the thing that kept the Nykaa app open between considered purchases, is now one tap away on an app the consumer was already using.

Blinkit and Zepto also have a financial incentive to accelerate this. Each additional adjacent category added to a grocery cart increases the basket size without increasing the delivery cost. They deliberately merchandise diapers, pet food, and beauty products next to vegetables. The grocery trip is the anchor. Everything else is margin.

Nykaa launched a 10-minute delivery pilot in Mumbai in October 2024. In response, a senior quick commerce executive said: “Certain low-priced items such as kajal pens, foundations or daily-use skincare items are finding traction on quick commerce — and platforms such as Nykaa stand to lose.”

Pet food is already a listed category on both Blinkit and Zepto. Zepto Pharmacy and Blinkit’s prescription medicine service launched within the same week in August 2025. Both move on high-frequency purchases. Both now have q-commerce to compete with. Which levers will they use to stay relevant? We’ll keep tabs and report back.

Hope this edition added value to your thought process. Do share this with your network.

This is probably a relatively new challenge a lot of D2C companies are facing today, but have you seen companies pivot product strategies to adapt to the new landscape? Are D2C brands only expected to survive in super-niches because product expansion means you're bound to compete with q-com?