Behind Astrotalk's ~₹12,500 Cr. IPO bet.

And why the shop matters more than the app for the IPO.

15,000 builders at MTW.

But a select group who are building, backing, and shaping the AI wave in India are meeting in secret at Speak Easy, Wispr Flow’s official after-hours. 50 spots. Most invites going out are 1:1. Few spots open. Want in?

Today’s edition.

Astrotalk does ₹1,214 Cr in revenue. It grows 85% year on year. Eight out of ten users come back without being asked. By every measure that matters, the business is working.

And yet, they built a shop. Why? Before we explore that, let’s take a step back and look at Astrotalk’s business.

The real runners in India’s $35B faith market.

One thing about India: it’s huge on astrology. Deciding on marriage dates, career moves, or even a child’s name? Indians will contact an astrologist first.

Estimates suggest that close to 80% of Indians consult an astrologer at some point, through family and relatives, and, as of 2025, even on their own. Plus, the market is growing.

GaneshaSpeaks saw it first in 2003.

It was built on telecom IVR — the right call in 2003, a trap by 2015. Their distribution ran through the telecom operator, which meant they never owned the user relationship. They couldn’t personalise. Couldn’t pivot.

Astroyogi made it to apps but stayed bootstrapped and conservative.

In FY25, when Astrotalk did ₹1,214 Cr, Astroyogi did ₹96 Cr.

AstroSage went the content route.

They generated enormous organic traffic, but almost no monetisation. They never solved the supply side, so the traffic sat earning ad rupees instead of consultation fees.

Here’s the thing.

Astrology runs on trust and referrals. You go to the astrologer your mother knows, or the one a neighbour vouches for. That trust is the product.

Solving the trust gap.

The standard playbook says: use the Beachhead Strategy.

Pick the smallest market you can win and expand from there. Reduce risk. Validate unit economics. Build a defensible position before going wide.

Astrotalk followed it, launching in Tier 2 and Tier 3 cities, targeting older consumers who’d openly consult an astrologer. Most didn’t move to the app. They already had someone they trusted down the street.

Think about it.

If consulting an astrologer was the norm, and you had one in your neighbourhood, someone your friends and family trust, would you willingly opt to consult with a new astrologer online?

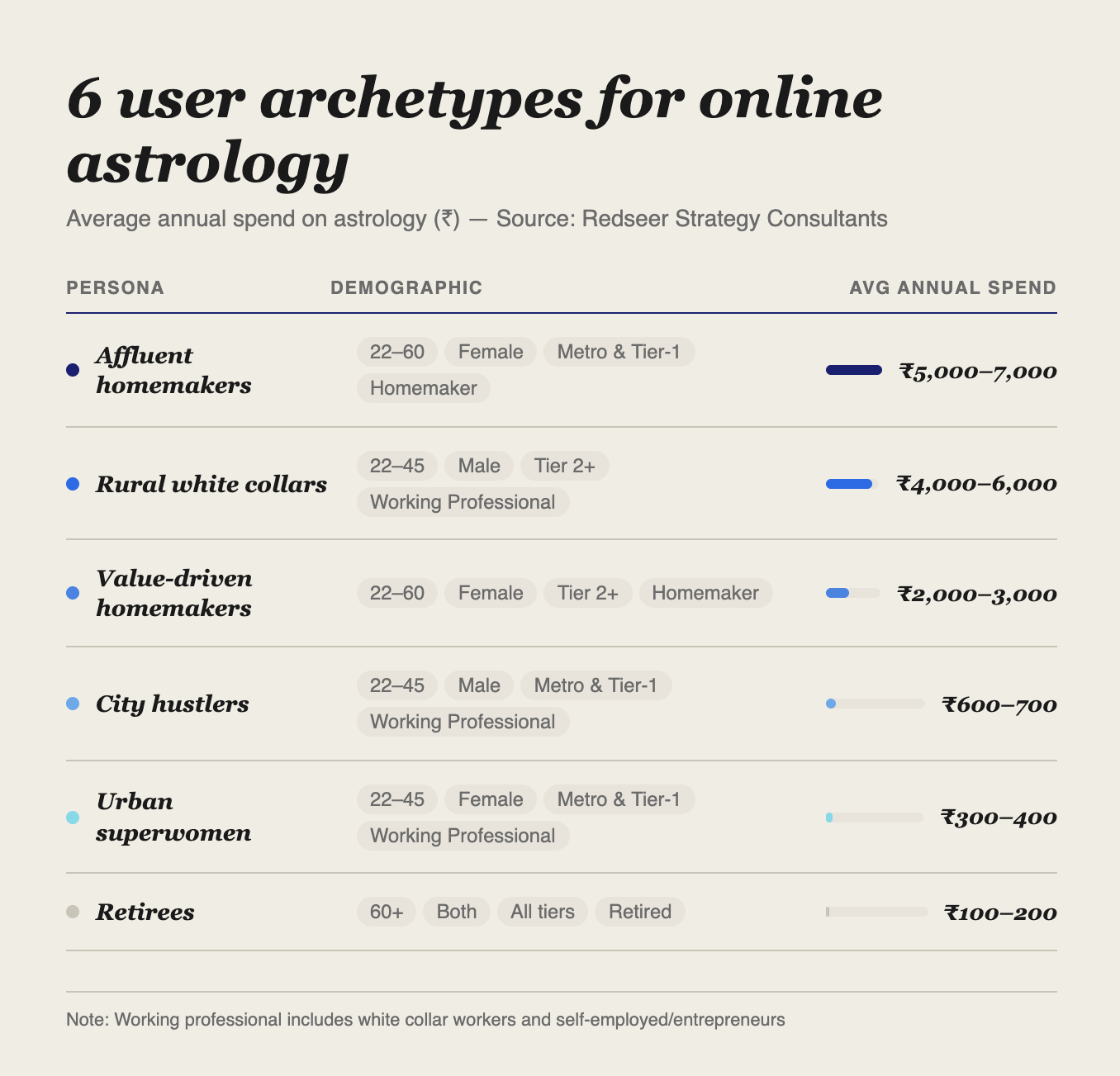

The users who showed up were the ones nobody had planned for. Young people in Tier 1 cities. 85% of Astrotalk’s revenue comes from users under 35, predominantly from metros.

Shame trumps trust and convenience.

Think like a 27-year-old, living away from family. You’ve got a problem you can’t talk about at work. An LDR that’s struggling. A career decision that’s keeping you up at night. You can’t call your mother. You can’t ask a friend — they’ll judge. The family astrologer back home is three states away, plus talking to them would mean your family would hear about it, too.

That’s a fundamentally different user. The product had to follow.

What started as a video platform became text-forward. Early users signalled a preference for audio over video. The team adjusted. Then came chat — WhatsApp-like, text-based, no camera, no trace. 65% of the business runs through it today. Video calls today essentially have no demand in the app.

Engineering trust in a market that runs on belief: the Airbnb insight.

The first thing customers want to see when they onboard into an astrology app is credible astrologers to actually solve their problems. Offline, this credibility comes from word of mouth. Online, it comes from curation and reviews.

Before acquiring a single user, Astrotalk compiled a list of roughly 15,000 qualified astrologers across India. The onboarding process consisted of five to seven rounds of interviews and accepted around 13% of applicants. No registration fee, unlike other platforms.

The logic was the same one that Airbnb used when it went door to door photographing host ap’ apartments before it had guests: the demand was already there, locked behind a trust problem. Solve supply first, make it credible, and the demand unlocks itself.

It did. Astrologers promoted themselves through personal social media channels and affiliate networks, bringing their existing audiences onto the platform. Supply became its own acquisition channel.

Astrotalk is profitable but has a margin cap.

To bring in one paying user, Astrotalk spends ₹575–870 on blended acquisition costs, lower than almost any other consumer app in India. According to co-founder Anmol Jain, the cost is recovered in six to eight months, with 80% of revenue coming from repeat customers. Demand renews due to unresolved anxieties and follow-ups, and revenue grows.

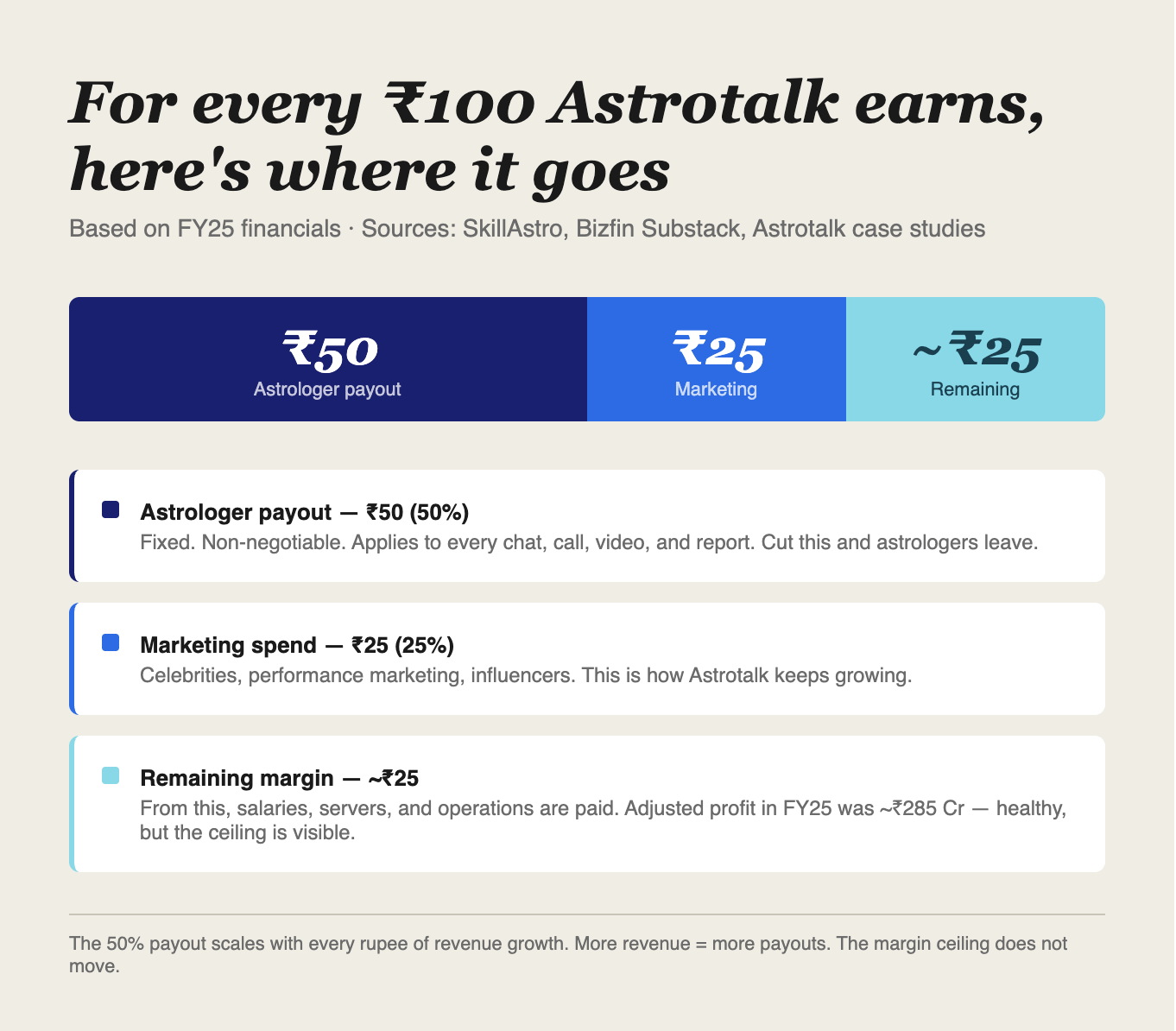

The model underneath is simple.

User pays per minute. Astrotalk keeps 50%. The astrologer keeps 50%. No exceptions across chat, call, video, or reports. No inventory, no logistics, no delivery. Consultation rates on the platform run from ₹20/min at entry level to ₹139/min for premium astrologers — the revenue scales with the astrologer's seniority, and so does the payout.

Except those numbers don’t move.

The 50% going to astrologers is structural. Touch it and the supply walks. And every time revenue grows, that payout grows in exact proportion.

The second constraint is harder to solve. The only way Astrotalk earns more is with more consultations. And more consultations mean more astrologer hours. There is no point at which adding one more user costs almost nothing.

Those aren’t good numbers for an IPO.

See, public markets do not price businesses on growth alone. They price them on the story; the margin structure tells about where the business goes from here. Astrotalk, which runs predominantly on consultations, will be valued like a services business, not a consumer brand where margins improve as a business scales.

This is precisely why it’s making the e-commerce pivot.

Astrotalk’s e-commerce store is really a bet to keep more margins.

When Astrotalk launched a store, the obvious play was for astrologers to recommend products during consultations. Buy a gemstone, get it shipped. A clean loop. In practice, only 3% of store revenue comes from astrologer recommendations. The remaining 97% arrives through brand recognition.

India’s religious and genuinely unorganised.

Gemstones prescribed during consultations worth tens of thousands of rupees. Rudraksha beads bought from temple-town vendors have no traceability. The Gem and Jewellery Export Promotion Council found that roughly 20% of jewellery sold in India is counterfeit or substandard. The problem is real.

And Astrotalks e-commerce store solves for it.

They built a supply chain to back it — raw materials sourced from Gujarat and West Bengal, batch testing and X-ray verification for rudraksha, each batch taking 10 to 50 days to clear. Stones certified by government laboratories, energised by astrologers before shipping.

There is a harder question underneath.

Astrotalk claims that 97% of store buyers arrive independently, without recommendations from astrologers. But independent of an explicit recommendation is not the same as independent of the platform entirely. A user who has consulted Astrotalk three times, trusts the brand, and then buys a bracelet from the store, is not an independent customer; they are an existing user buying conveniently within an ecosystem they already live in.

Besides, Tier 2 and Tier 3 buyers who already purchase spiritual products locally, at lower prices and with the tactile reassurance of seeing the product before buying, have no obvious reason to switch to a premium online store unless the brand trust is strong enough to override both price and habit. Whether it is, and whether that holds at the ₹400 Cr ARR scale, is not answered by the current numbers.

The numbers are impressive, though.

1.6 million orders in 2025, ₹140 Cr in revenue, ARR above ₹200 Cr. Repeat purchase rate: 24%. A separate operation entirely. It’s browser-led, website-first, run by its own team of 50 to 60 people. No astrologer payout. And it all started with a ₹30 lakh sum.

Astrotalk’s e-commerce arm is targeting ~₹400-500 Cr in ARR by FY27. To get there, Astrotalk is simultaneously running a consultation marketplace, ecommerce operations, offline retail, and gemstone sourcing. Those are four businesses with entirely different supply chains, economics, and management demands.

The store is tracking in the right direction. Whether the buyers are truly new to the ecosystem or simply existing users buying more conveniently, whether certification trust is real or brand familiarity is doing all the work, whether the IPO story holds when investors ask these same questions — none of that is settled yet. The DRHP will be the first honest test of whether the market believes it.

Is there no scenerio when Astrotalk becomes a strong marketplace and squeezes the astrologer to take home less? Like Amazon does with its suppliers.

Private label play - can astrotalk hire a new generation of astrologers by giving them certificates etc, truning into an university sorts for such courses, earning in Ed-tech

Can Astrotalk make AI astrologer so real life that it earns and consumes less token-money than real life astrologer? This may be highly scalable also.

Can Astrotalk make astrologer business line as Loss-leader for top funnel acquisition, and grow it's ecomm business to 20X in cross sell and upsell?

Good explanation.