0 ships built. ₹4,780 crore in orders. How?

How India's biggest shipyard does business.

How does a shipyard with a dry dock shipbuilding capacity of 400,000 tonnes (~3X that of any other Indian shipyard) and 3 owners earn no profit over 3 decades?

Nikhil Gandhi’s SKIL Group built the Pipavav shipyard, then ran up over ₹6,000 crore in debt, while a ₹2,975-crore Navy patrol vessel order remained unfinished. Then, Anil Ambani’s Reliance took over in 2015, chasing a ₹28,680 Cr. warship program on top of it, and pushed total debt past ₹12,000 Cr.

Now Nikhil Merchant’s Swan Defence and Heavy Industries (SDHI) owns it, and shipbuilding has officially restarted. Will the third time actually be the charm?

1 month of Granola free. Start today.

We’ve tried several AI note-takers at GrowthX, and Granola has been our go-to for the past year. It gives us comprehensive prep notes before every meeting, near-accurate transcripts, and even makes follow-up tasks like emails and planning easy. Try Granola Pro free for 1 month by signing up using the link below.

Fact: Shipbuilding is an ‘anti-business’.

Ideally, a business should turn capital into more capital. Shipbuilding almost always doesn’t.

See, first, you build the factory.

The dry dock, the cranes, kilometres of fabrication sheds. Just the dry dock at Pipavav, India’s largest, cost ₹330 crore to build. Then, even once the yard is running, a ship itself takes years to build, and gets paid for in stages: a third at keel-laying, a chunk at launch, the rest only at delivery.

Next up, the contracts.

Your earnings go either way depending on the type of contracts you engage in. Commercial contracts are typically fixed-price, agreed before construction starts. So, if steel costs rise mid-build, and over a multi-year contract they usually do, the shipbuilder eats the difference.

Even a well-run, diversified player like L&T can’t escape that math. Its shipbuilding-adjacent defence segment posted a margin as low as 8.3% in one recent quarter, down from 13.6% a year earlier.

Defence contracts, on the other hand, could work differently, with costs shared or passed through too.

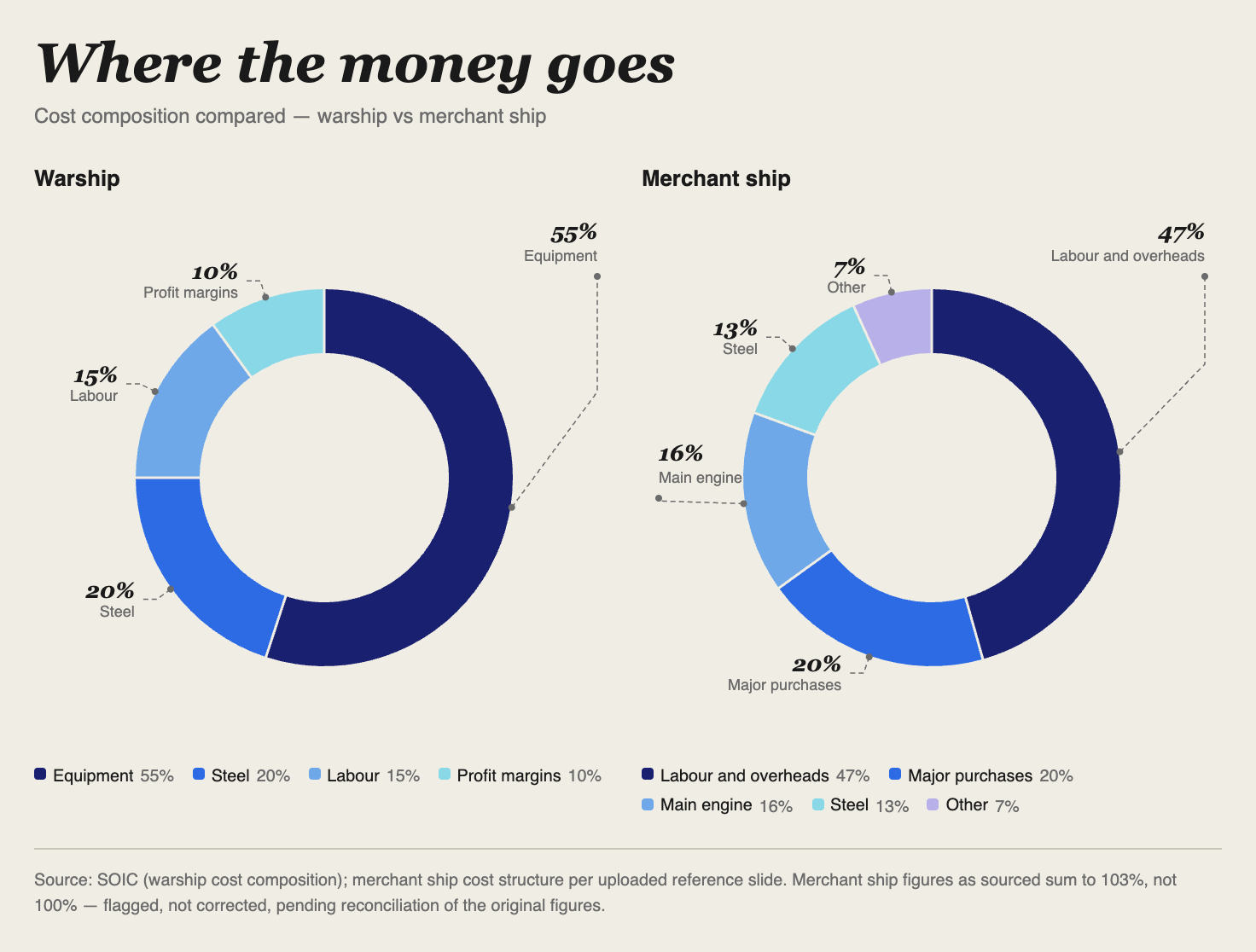

Plus, the margins also depend on what you’re building, not just when. A bulk carrier is a simpler, lower-margin build. A warship or an LNG carrier carries far more specialised engineering and a cost structure to match. Often, the equipment alone costs a fraction of the shipping costs.

So, why do shipyards keep building?

Because the government is betting heavily on them.

Two reasons:

1. Trade

Even today, India carries less than 5% of its own trade on its own ships. That gap costs roughly ₹7.17 lakh crore ($75 billion) a year in freight, paid to whoever owns the ship — right now, that’s almost always a foreign company.

See, no major trading nation carries all its own cargo on its own ships either. Using the global charter market is normal, often efficient. India’s current target is modest: re-flag around 300 foreign-owned ships by 2030, a small dent in a very large gap.

How? More Indian-flagged ships mean more of that freight revenue lands with Indian companies rather than foreign ones, even if the ship itself was built abroad and the fuel is still imported.

2. Political power

The navy controls the sea lanes, deters anyone who’d threaten them, and protects the trade that already depends on them.

China’s navy now counts over 350 vessels, more than any other country’s, with a stated target of 450 by 2030, and has maintained a presence in the Indian Ocean since 2008.

For India, that’s a threat. Over 7,500 kilometres of coastline sit almost directly across those same sea lanes.

Those reasons combined are why India has a 300-ship target by 2047 and 25% capital assistance for brownfield shipyards today.

What’s in it for a shipyard operator?

For a PSU, the answer is straightforward.

Cochin and Goa’s order books are 66% and 78% Navy respectively all thanks to assured, government-guaranteed demand. Since defence customers pay in milestone advances, effectively pre-funding construction, there’s zero external debt. Even a bad quarter is just a bad quarter, because the state stands behind the balance sheet either way.

Now compare that with a private operator.

The answer to the above question is: not a lot, and not much, on its own.

L&T’s shipbuilding arm had a negative net worth the last time it reported as a standalone entity, before L&T folded it into the parent company specifically to stop rivals using its weak financials against it in bidding. Chowgule’s dedicated shipbuilding subsidiary posts a negative operating margin today, kept alive only by equity injections from its much larger, unrelated parent group. Strip away a bigger sibling business willing to absorb the losses, and there is no clean example in India of a shipyard that is both genuinely private and genuinely profitable on shipbuilding alone.

So why does SDHI own Pipapav again?

Four reasons:

1. They got a steal deal.

Swan paid ~₹2,108 crore for a shipyard that would cost between ₹15,000 crore (a single new 0.5 million GT greenfield yard, per the government’s own estimate) and ₹45,000 crore (Cochin’s new joint facility with HD Hyundai) to build from scratch. All they needed to do was replace old parts. Why? Because the yard came out of insolvency, not the open market. (They still had to spend ~₹2390 Cr. to revive the facility).

2. The expansion deal was smooth.

When SDHI wanted to expand Pipavav’s capacity — new slipways, jetties, cranes, dredging, and block fabrication facilities, plus staff training and a 200-acre maritime cluster - it didn’t have to start from zero.

Why? Swan had spent over a decade working with the Gujarat Maritime Board on its LNG terminal down the coast, and that same relationship now serves as the channel for a ₹4,250 crore shipyard expansion MoU — a regulator Swan didn’t need to build trust with from scratch.

3. They get massive subsidies for building ships.

SBFAS hands back 15-25% of every ship’s contract value as a straight cash grant. More subsidies = more money added to the contract price.

4. Shipbuilding is the start of SDHI’s expansion plan.

See, the dry dock, cranes and fabrication sheds that build a ship can build almost anything else heavy and steel-based: port cranes, offshore platforms, industrial structures. No wonder SDHI’s next move is to enter the crane and port equipment manufacturing business, according to the company’s CEO, Vipin Kumar Saxena.

The catch? Nobody subsidises a crane factory. The government funds ships, specifically. Put simply, shipbuilding is only the subsidised entry ticket — the one category of heavy fabrication the state will help pay for, unlocking a physical platform a thin shipbuilding margin alone would never justify owning outright.

Can customers trust a twice-bankrupt yard to build again?

Yes, it turns out. Provided it could show proof of finishing work on time.

SDHI took on 20 repair and refit projects.

Why? This would be proof that the company could commit to its deadlines.

The projects included Coast Guard vessels, offshore oil and gas assets, tugs, accommodation barges — delivered on schedule or ahead of it, per CEO Vipin Kumar Saxena.

Next, the company built backwards into its supply chain.

See, the SDHI applied for the SBFAS (Shipbuilding Financial Assistance Scheme). Accordingly, the company had to develop local component manufacturing capabilities to avail the grant. Import the components, and the subsidy shrinks or disappears.

Newbuild contracts came last. But they came strong.

Six chemical tankers for Norway’s Rederiet Stenersen (₹2,171 Cr.), four ammonia dual-fuel bulk carriers for Energy ONE (₹2,581 Cr., India’s first ammonia-fuelled ship order), a defence export for Oman’s navy, and a batch of rusted OSV hulls, abandoned mid-build for a decade, finally finished for a new buyer.

Competitive pricing was one reason. It’s not that SDHI’s ships were cheaper to build. The government just bore a fraction of the cost. (China, Korea and Japan built their shipbuilding capacities the same way in the early years).

The other reason? Korean and Chinese yards are booked solid into 2028. Global order books are at a 17-year high — ageing tanker fleets need replacing, and the shift to LNG- and ammonia-powered ships is pulling in fresh demand faster than anyone can build to meet it. When the two biggest shipbuilding nations on earth have no open slots, buyers stop asking who’s cheapest and start asking who’s available.

Right now, that’s India.

What’s next for SDHI?

SDHI’s Q4 FY26 operating margin: -105.98%. Two possible explanations for that.

One: the yard is pre-revenue on the contracts that matter. Its newbuild deals were signed too late to count — Stenersen in January, Energy ONE in April, after the year had already closed. The ₹440 crore that did land came almost entirely from repair work, by simple timing, not by SDHI’s own account.

Two: even once milestones start paying out, the core business doesn’t clear a profit.

Nobody can say which yet. We’ll know for sure only in 2028.

Want to plug your brand into our newsletter?

Email us at collab@growthx.club

Can you guys please

Break it down more detailed into simpler words so that it would be easy to understand for anyone

Am unable to get anything